Stock (Symbol) |

NVIDIA (NVDA) |

Stock Price |

$481 |

Sector |

| Technology |

Data is as of |

| December 13, 2023 |

Expected to Report |

| February 21 |

Company Description |

NVIDIA Corporation is a personal computer (PC) gaming market. NVIDIA Corporation is a personal computer (PC) gaming market.

The Company’s segments include Graphics and Compute & Networking. The Graphics segment includes GeForce graphics processing units (GPUs) for gaming and PCs, the GeForce NOW game streaming service and related infrastructure, and solutions for gaming platforms; Quadro/NVIDIA RTX GPUs for enterprise workstation graphics; virtual GPU software for cloud-based visual and virtual computing; automotive platforms for infotainment systems, and Omniverse software for building three-dimensional (3D) designs and virtual worlds. The Compute & Networking segment includes Data Center platforms and systems for artificial intelligence (AI), high-performance computing (HPC), and accelerated computing; Mellanox networking and interconnect solutions; automotive AI Cockpit, autonomous driving development agreements, and autonomous vehicle solutions; cryptocurrency mining processors (CMP); Jetson for robotics, and NVIDIA AI Enterprise. Source: Refinitiv |

Sharek’s Take |

NVIDIA (NVDA) stock has jumped from $146 to $481 so far in 2023. And although the stock seems high, it still could double in price in 2024. The reason NVDA’s stock should go up is profits are zooming higher. Profits (in earnings per share or EPS) are expected to rise from $12.29 this year to $20.50 in 2024. NVDA currently has a 39 P/E, and thus sells for 39 x $12.29 = $481. In 2024 I think it it could be 45 x $20.50 = $923. In addition profit estimates have been rising. During the past 4 qtrs 2024 estimates have gone from $5.87 to $10.38, $16.70 and now $20.50. NVDA coud realistically make $25 in profits in 2024. If it did so and got a 40 P/E it would be a $1000 stock. NVIDIA (NVDA) stock has jumped from $146 to $481 so far in 2023. And although the stock seems high, it still could double in price in 2024. The reason NVDA’s stock should go up is profits are zooming higher. Profits (in earnings per share or EPS) are expected to rise from $12.29 this year to $20.50 in 2024. NVDA currently has a 39 P/E, and thus sells for 39 x $12.29 = $481. In 2024 I think it it could be 45 x $20.50 = $923. In addition profit estimates have been rising. During the past 4 qtrs 2024 estimates have gone from $5.87 to $10.38, $16.70 and now $20.50. NVDA coud realistically make $25 in profits in 2024. If it did so and got a 40 P/E it would be a $1000 stock.

NVIDIA was originally focused on the computer graphics market, and invented the first graphics processing unit (GPU) in 1999 and made the company the leader in computer graphics. The company introduced its CUDA programming model in 2006 and ushered in parallel processing of its GPU for high-performance computing that could be used in fields including aerospace, biotechnology, and energy exploration. NVDA has since expanded its architecture to scientific computing, artificial intelligence, data science, autonomous vehicles, robotics, and virtual reality (or AR). NVIDIA’s rapid growth is driven by its Data Center segment, due to the strong demand for the HGX platform which runs Generative AI and large language models. Generative AI can do more than understand text and numbers. The computer can try to understand your words to program itself. And the NVIDIA GDX platform is most robust AI platform today. It’s the world’s first AI supercomputer. AI applications built on NVIDIA include ChatGPT, Microsoft 365 Copilot, ServiceNow’s Now Assist and Adobe Firefly. Here’s how it works:

NVDA has four operating segments : Gaming, Data Center, Professional Visualization and Automotive. Here are segment stats from last qtr:

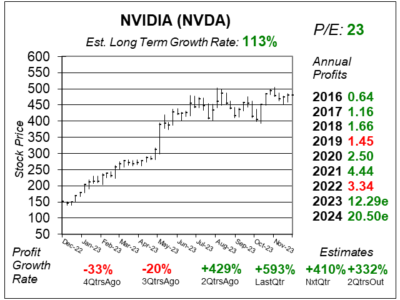

NVIDIA is in a golden era of a universal upgrade in computing. The company breaks down the four previous eras as (1) PC lead by IBM, (2) Internet, (3) Mobile & Cloud lead by the iPhone, and (4) AI. I consider NVDA a rapid grower, which in my opinion is a company growing year-over-year profits 65% or greater. Analysts give NVDA an Estimated Long Term Growth Rate of 113%. Management even buys back stock and pays a small dividend. In 2022, management returned $10.44 billion in stock buybacks and cash dividends. But the dividend is just $0.04 per share. NVIDIA is part of the Growth Portfolio and Aggressive Growth Portfolio. I will add to my position as I feel this stock has the most upside for 2024. |

One Year Chart |

NVDA has been basing since May. That’s 6 months for what was perhaps the hottest stock in the US earlier this year. That’s a good rest. Now the stock is poised for another run higher. NVDA has been basing since May. That’s 6 months for what was perhaps the hottest stock in the US earlier this year. That’s a good rest. Now the stock is poised for another run higher.

Since we are in NVDA’s Fiscal Q4, I’m calculating the P/E in this chart using 2024 profit estimates. That makes the P/E just 23! Last quarter the P/E was 46! Quarterly profits are surging higher. And that’s expected to continue the next two qtrs. The Est. LTG is 113%. The Est. LTG is analysts’ 3-5 year guess of annual profit growth (not stock growth). |

Earnings Table |

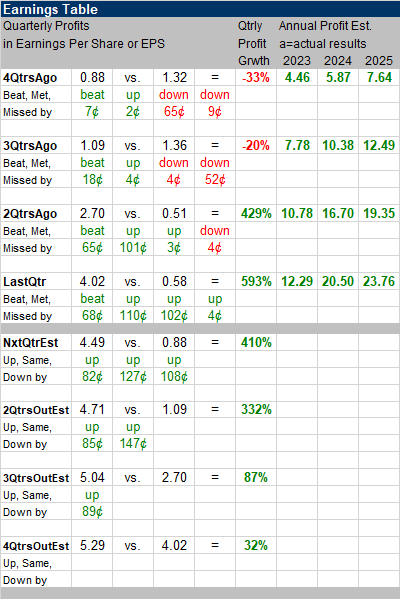

Last qtr, Nvidia reported 593% profit growth and beat estimates of 476% growth. Revenue grew 206% and beat estimates of 171%. Gross margin expanded to 74.0% from 53.6% last year due to higher Data Center sales. During the past 4 qtrs qtrly profits have gone from $0.88 to $1.09 to $2.70 and now $4.02. Last qtr, Nvidia reported 593% profit growth and beat estimates of 476% growth. Revenue grew 206% and beat estimates of 171%. Gross margin expanded to 74.0% from 53.6% last year due to higher Data Center sales. During the past 4 qtrs qtrly profits have gone from $0.88 to $1.09 to $2.70 and now $4.02.

In the earnings release management stated large language model startups, consumer internet companies (Meta) and global service providers were the first AI movers, and the next waves will be nations, regional service providers, and enterprise software companies (Adobe, ServiceNow) adding AI copilots and assistants to their platforms. A vast majority of last qtr’s revenue was from the NVIDIA HGX platform based on the Hopper GPU versus the prior generation Ampere GPU. Annual Profit Estimates continue to climb. Looking at 2024 numbers, what do you think the company will actually make? Qtrly Profit Estimates for the next 4 qtrs are 410%, 332%, 87%, and 32%. For next qtr, analysts predict revenue will climb 231% year-over-year. |

Fair Value |

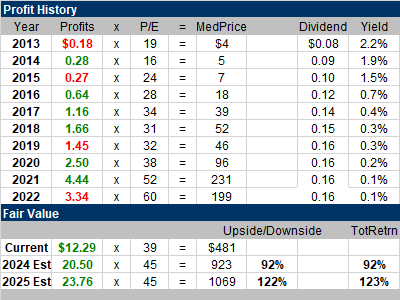

Note this stock sells has a P/E of 39, or sells for 39x 2023 profit estimates of $12.29. Last quarter, NVDA had a P/E of 46. My Fair Value is a P/E of 45. This gives me a Fair Value of $923 in 2024. That would be a 92% gain from here. And recall 2024 profit estimates have been jumping higher. |

Bottom Line |

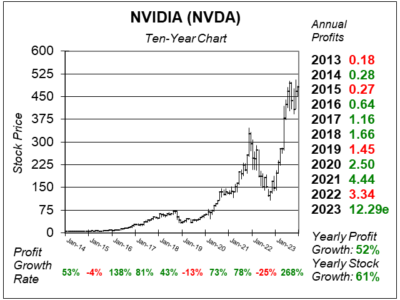

NVIDIA (NVDA) stock has had a rocky decade. During 2016 the NVDIA GeForce video processor created a surge in revenue and profits and helped the stock soar from $8 to $27 that year. NVIDIA continued to rise into 2018 and peaked at $73. Then the stock fell in late-2018 as the company had lots of returns of its high-end processors as the price of Bitcoin declined and cryptoy miners returned their gear back to NVDA. Note profits fell in 2019. The 2022 slump was due to a downturn in sales in the Gaming division as (1) businesses were flush with cash in 2021 and had already upgraded computers and (2) Bitcoin miners found it unprofitable to mine with lower crypto prices combined with high electricity costs. AI has ushered in a new round of spending for advanced computers. and NVIDIA has a clear lead on the brains for this technology. It’s hard to fathom what this company’s revenue, profits, and even stock price could be in the coming years. NVDA will move from 3rd to 1st in the Growth Portfolio Power Rankings. The stock will jump from 7th to 1st in the Aggressive Growth Portfolio Power Rankings. |

Power Rankings |

Growth Stock Portfolio

1 of 33Aggressive Growth Portfolio 1 of 16Conservative Stock Portfolio N/A |