Stock (Symbol) |

Salesforce.com (CRM) |

Stock Price |

$219 |

Sector |

| Technology |

Data is as of |

| September 13, 2023 |

Expected to Report |

| November 28 |

Company Description |

Salesforce is a provider of customer relationship management (CRM) platform. Salesforce is a provider of customer relationship management (CRM) platform.

Its Customer 360 platform delivers a source, which connects customer data across systems, applications and devices to help companies sell, service, market and conduct commerce from anywhere. It focuses on cloud, mobile, social, analytics and artificial intelligence, which connect to its customers and enable companies to transform their businesses. It also enables third parties to use its platform and developer tools to create additional functionality and applications that run on its platform. Its customers use its sales offering to store data, monitor leads and progress, forecast opportunities, gain insights through analytics and relationship intelligence and deliver quotes, contracts and invoices. Its service offering helps to connect its service agents with customers across any touchpoint. It helps customers to resolve routine issues with predictions and recommendations. Source: Refinitiv |

Sharek’s Take |

Salesforce (CRM) enjoyed its second consecutive qtr in which its operating margin grew more than 10 percentage points. Last quarter, CRM’s non-GAAP operating margin expanded to 31.6% in the last qtr from 19.9% last year. Management did not expect 30% operating margins until three quarters from now. Improvements in the margin were driven by the company’s rightsizing efforts, strong revenues, and investment timing. With the help of these expanding margins, the company delivered great results last qtr as profits jumped 78% while revenue grew 11%. Salesforce (CRM) enjoyed its second consecutive qtr in which its operating margin grew more than 10 percentage points. Last quarter, CRM’s non-GAAP operating margin expanded to 31.6% in the last qtr from 19.9% last year. Management did not expect 30% operating margins until three quarters from now. Improvements in the margin were driven by the company’s rightsizing efforts, strong revenues, and investment timing. With the help of these expanding margins, the company delivered great results last qtr as profits jumped 78% while revenue grew 11%.

Salesforce is the world’s leader in customer relationship management (CRM) software and connects more than 150,000 clients to their customers via the internet and stores this customer information in the cloud. The company had more than 73,000 employees as of January 31, 2022. Salesforce boasts the #1 Sales Cloud, #1 Service Cloud, #1 Marketing Cloud, #1 CRM platform, and #1 integration software in Mulesoft. The company is large but continues to grow at a healthy rate due to acquisitions including Tableau, Mulesoft, and Slack. Salesforce is a perfect fit for AI and that should bring more opportunity to grow revenue in the years ahead. Here’s a breakdown of the company’s service offerings:

Salesforce used to be a rapid grower, and has now had its revenue growth simmer down as the company’s gotten exponentially larger. Much of Salesforece’s growh has come from acquisitions, which is fine by me. But now that the company is an Enterprise, big aquisitions might not make as much of an impact on profits. Still, analysts have 26% Estimated Long Term Growth Rate on the stock, which I think is overly optimistic. CRM doesn’t pay a dividend, but management has a stock buyback program in place. In 2022, management bought back $4 billion in stock, but since this is a software company that offers a lot of stock options for employees, shares outstanding didn’t drop much. I’m very excited about Salesforce becoming a force in AI, and will cover this more in future reports. CRM is on the radar for the Growth Portfolio. I think the stock is fairly valued here, and would be tempted to buy it if the stock were to dip due to poor stock market conditions. |

One Year Chart |

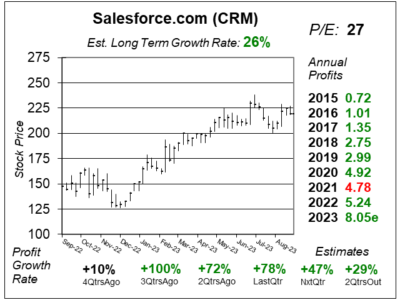

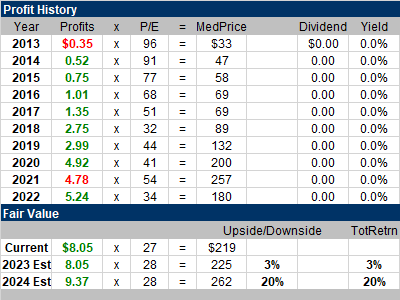

The one-year chart looked terrible a year ago, but now looks to be in great shape, having gained an upward momentum that began as the year started. The Est. LTG is 26% this qtr. That’s up from 23% last quarter. Profits are good now because the company is penny-pinching. What will profit growth slow to? Maybe 15%? The P/E of 27 is down from 29 last qtr. My Fair Value is a P/E of 28. Qtrly profit growth looks good! Estimates as well! |

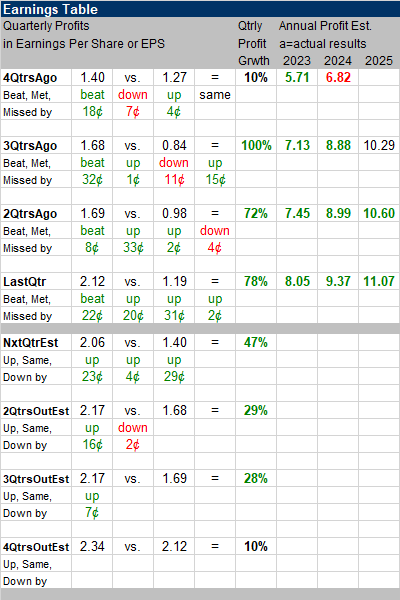

Earnings Table |

Last qtr, Salesforce delivered 78% profit growth and beat expectations of 60% growth. Revenue increased 11%, same with 2QtrsAgo and in line with analyst expectations. The current remaining performance obligation grew by 12%. Revenue geographically speaking: Last qtr, Salesforce delivered 78% profit growth and beat expectations of 60% growth. Revenue increased 11%, same with 2QtrsAgo and in line with analyst expectations. The current remaining performance obligation grew by 12%. Revenue geographically speaking:

Growth was driven by Service Cloud and Data Cloud, particularly with MuleSoft which enjoyed great business wins. Almost half of all deals greater than $1 million included MuleSoft. Einstein, the world’s first generative AI for a CRM platform, is also seeing strong customer momentum. Overall revenue growth was partially offset by continuing weakness in professional services. The company also continues to experience elongated sales cycles and deal compression. But in terms of industry verticals, manufacturing, automotive, and energy are exhibiting great resilience amid the measured macro environment. Annual recurring revenue for eight of Salesforce’s industry cloud solutions grew more than 50%. US business wins include SiriusXM , KPMG, FedEx, Schneider Electric, and PenFed. International business wins include Hargreaves Lansdown; the Department of Education in Victoria, Australia; and Banco Carrefour. Annual Profit Estimates are up again this qtr. For 2024, management expects revenue to grow by around 11%, driven by strength in subscription and support revenue, particularly for MuleSoft. Qtrly Profit Estimates are for 47%, 29%, 28%, and 10% profit growth in the next 4 qtrs. For next quarter, nalysts expect revenue to grow 11% once again. |

Fair Value |

My Fair Value P/E is 28 this quarter, down from 30 last quarter. My Fair Value P/E is 28 this quarter, down from 30 last quarter.

The stock seems fairly valued here, with 20% upside for next year. Note, CRM has been increasing annual profit estimates. CRM has a January 31 fiscal year-end. |

Bottom Line |

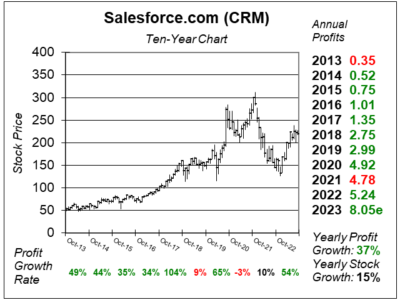

Salesforce (CRM) had been a solid stock this last decade. The shares corrected in 2022, and that decline was too harsh, so the stock has rallied higher this year. I blew a grand opportunity to buy the stock in January this year when the stock was $136.Tech stocks sold off in December 2022 due to tax loss selling and investors capitulating from a Bear Market. Salesforce (CRM) had been a solid stock this last decade. The shares corrected in 2022, and that decline was too harsh, so the stock has rallied higher this year. I blew a grand opportunity to buy the stock in January this year when the stock was $136.Tech stocks sold off in December 2022 due to tax loss selling and investors capitulating from a Bear Market.

Salesforce has done a phenomenal job cutting csts and increasing profit marggins. And the overall business environment has been good considering the sluggish economy. AI will bring great innovations to this company and its customers. CRM is on the radar for the Growth Stock Portfolio. I’d look to add the stock on a dip in price. |

Power Rankings |

Growth Stock Portfolio

N/AAggressive Growth Portfolio N/AConservative Stock Portfolio N/A |