Stock (Symbol) |

Becton Dickinson (BDX) |

Stock Price |

$204 |

Sector |

| Healthcare |

Data is as of |

| September 11, 2017 |

Expected to Report |

| Nov 1 |

Company Description |

BDX is a global medical technology company engaged in the development, manufacture and sale of a range of medical supplies, devices, laboratory equipment and diagnostic products used by healthcare institutions, life science researchers, clinical laboratories. The Company operates through two segments: BD Medical and BD Life Sciences. Source: Thomson Financial BDX is a global medical technology company engaged in the development, manufacture and sale of a range of medical supplies, devices, laboratory equipment and diagnostic products used by healthcare institutions, life science researchers, clinical laboratories. The Company operates through two segments: BD Medical and BD Life Sciences. Source: Thomson Financial |

Sharek’s Take |

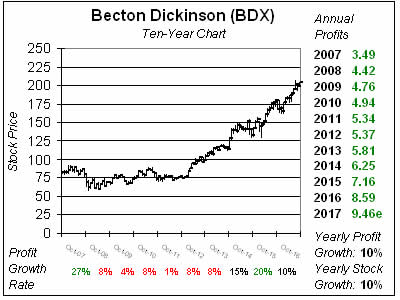

Becton Dickinson (BDX) is acquiring C.R. Bard (BCR), and the deal is expected to close by the end of the year. The deal merges two 100 year old companies with long histories of providing equipment to hospitals, and delivering investors with double-digit returns for many years. Becton Dickinson has manufactured syringes, catheters, lab equipment, diagnostic tests, and other disposable items for hospitals since 1897. The company has been a perennial 8% to 10% grower, unless it makes a big acquisition that causes profits to surge like in 2015 when it acquired CareFusion, a maker of precision drug dispensing equipment. CareFusion gave Becton, Dickinson a more complete menu of medical products to hospitals and Becton can also use its deep International network to sell CareFusion products. And now C.R. Bard, which was founded in 1907, takes things to a whole other level with its catheters and stents. BDX is a very safe stock that has produced growth around twice the rate of the S&P 500. It possesses an Est. LTG of 10% per year in addition to a 2% yield. The company has a history of growth dating back a century, and a dividend that’s been raised for close to 50 years. Profits have grown/are expected to grow from approximately $8.50 last year to $9.50 this year, $10.50 next year and $11.50 in 2019. BDX stock sells for around 20x earnings, a reasonable price for a quality long-term investment. Becton Dickinson (BDX) is acquiring C.R. Bard (BCR), and the deal is expected to close by the end of the year. The deal merges two 100 year old companies with long histories of providing equipment to hospitals, and delivering investors with double-digit returns for many years. Becton Dickinson has manufactured syringes, catheters, lab equipment, diagnostic tests, and other disposable items for hospitals since 1897. The company has been a perennial 8% to 10% grower, unless it makes a big acquisition that causes profits to surge like in 2015 when it acquired CareFusion, a maker of precision drug dispensing equipment. CareFusion gave Becton, Dickinson a more complete menu of medical products to hospitals and Becton can also use its deep International network to sell CareFusion products. And now C.R. Bard, which was founded in 1907, takes things to a whole other level with its catheters and stents. BDX is a very safe stock that has produced growth around twice the rate of the S&P 500. It possesses an Est. LTG of 10% per year in addition to a 2% yield. The company has a history of growth dating back a century, and a dividend that’s been raised for close to 50 years. Profits have grown/are expected to grow from approximately $8.50 last year to $9.50 this year, $10.50 next year and $11.50 in 2019. BDX stock sells for around 20x earnings, a reasonable price for a quality long-term investment. |

One Year Chart |

Last qtr BDX had -5% sales growth, but that was because it sold off a division (Sales would have grown 2%). Profit growth was 5% which beat estimates of 4% growth. Annual estimates got bumped up slightly this qtr and qtrly profit estimates stayed about the same. Analysts Estimate profit will grow 12%, 5%, 6% and 10% the next 4 qtrs. The Est. LTG of 10% is good considering this is a top-notch stock for safety, and the company pays a 2% yield. Last qtr BDX had -5% sales growth, but that was because it sold off a division (Sales would have grown 2%). Profit growth was 5% which beat estimates of 4% growth. Annual estimates got bumped up slightly this qtr and qtrly profit estimates stayed about the same. Analysts Estimate profit will grow 12%, 5%, 6% and 10% the next 4 qtrs. The Est. LTG of 10% is good considering this is a top-notch stock for safety, and the company pays a 2% yield. |

Fair Value |

My Fair Value is 21x earnings, which gives us a Fair Value of $219 a share. Since Becton Dickinson reports its fiscal year end September 30th, I’m looking ahead to next year’s estimates at this time. My Fair Value is 21x earnings, which gives us a Fair Value of $219 a share. Since Becton Dickinson reports its fiscal year end September 30th, I’m looking ahead to next year’s estimates at this time. |

Bottom Line |

Becton, Dickinson is one of the safest stocks out there, and now with C.R. Bard the company will be even stronger with an enormous catalog of healthcare instruments and supplies that are used by hospitals every day. BDX has been in business more than a century and has raised its dividend for close to 50 years. During the last decade BDX has growth its profits 10% a year, and the stock has grown 10% a year as well — while paying a 2% yield. Plus, C.R. Bard could provide cost savings that increase profits better than analysts expect. BDX ranks 21st in the Conservative Portfolio Power Rankings. Becton, Dickinson is one of the safest stocks out there, and now with C.R. Bard the company will be even stronger with an enormous catalog of healthcare instruments and supplies that are used by hospitals every day. BDX has been in business more than a century and has raised its dividend for close to 50 years. During the last decade BDX has growth its profits 10% a year, and the stock has grown 10% a year as well — while paying a 2% yield. Plus, C.R. Bard could provide cost savings that increase profits better than analysts expect. BDX ranks 21st in the Conservative Portfolio Power Rankings. |

Power Rankings |

Growth Stock Portfolio

N/AAggressive Growth Portfolio N/AConservative Stock Portfolio 21 of 33 |