Stock (Symbol) |

CVS Caremark (CVS) |

Stock Price |

$74 |

Sector |

| Food & Necessities |

Data is as of |

| November 19, 2016 |

Expected to Report |

| Feb 7 – 13 |

Company Description |

CVS operates through three business segments: Pharmacy Services, Retail Pharmacy and Corporate. The Pharmacy Services provides a range of pharmacy benefit management (PBM) services and operates under the CVS/caremark Pharmacy Services, Novologix and Navarro Health Services names. The Retail Pharmacy sells prescription drugs and an assortment of general merchandise, including over-the-counter drugs, beauty products and cosmetics, personal care products, convenience foods, photo finishing, seasonal merchandise and greeting cards through the Company’s retail stores, online retail pharmacy Websites and retail healthcare clinics. The Corporate provides management and administrative services to support the overall operations of the Company. The Company, through its wholly owned subsidiary, Omnicare, Inc., provides pharmacy services to long-term care facilities. Source: Thomson Financial CVS operates through three business segments: Pharmacy Services, Retail Pharmacy and Corporate. The Pharmacy Services provides a range of pharmacy benefit management (PBM) services and operates under the CVS/caremark Pharmacy Services, Novologix and Navarro Health Services names. The Retail Pharmacy sells prescription drugs and an assortment of general merchandise, including over-the-counter drugs, beauty products and cosmetics, personal care products, convenience foods, photo finishing, seasonal merchandise and greeting cards through the Company’s retail stores, online retail pharmacy Websites and retail healthcare clinics. The Corporate provides management and administrative services to support the overall operations of the Company. The Company, through its wholly owned subsidiary, Omnicare, Inc., provides pharmacy services to long-term care facilities. Source: Thomson Financial |

Sharek’s Take |

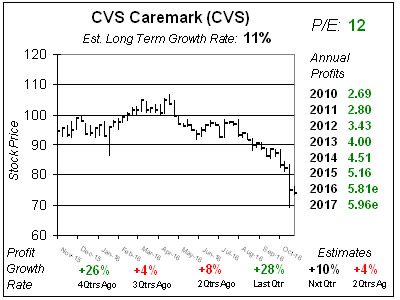

In a shocking turn of events, CVS Caremark (CVS) said it is losing 40 million prescriptions next year and slashed its 2017 profit guidance. CVS is made up of CVS drugstores and Caremark, a pharmacy benefit manager (PBM) that buys drugs in bulk then passes the savings along to its clients. Competition in the PBM space has heated up recently, with UnitedHealth’s OptumRX division taking deals it wouldn’t have in the past. Now the loss of 40 million scripts to Walgreens Boots took down 2017 profit growth estimates from 12% to 3% and more importantly cast a cloud over the ability for PBMs to grow profits in the future. CVS is a good stock, having grown profits every year since 2002. Management is savvy and buys back stock in addition to making smart acquisitions. In 2007 CVS acquired Caremark, a PBM that was/is growing 20% a year and in May 2015 acquired Omnicare, a PBM for seniors. One month later it purchased Target’s pharmacy business of 1600 drugstores. The recent developments have slashed CVS’s Estimated Long-Term Growth rate from 15% a year to 11%. I will sell CVS from the Growth Portfolio as the Est LTG is below the 15% I look for and I think feel this stock will be down here for a while with 2017’s profits are expected to grow just 3%. I will continue to stick with CVS in the Conservative Portfolio as this is a safe stock with a yield north of 2%. In a shocking turn of events, CVS Caremark (CVS) said it is losing 40 million prescriptions next year and slashed its 2017 profit guidance. CVS is made up of CVS drugstores and Caremark, a pharmacy benefit manager (PBM) that buys drugs in bulk then passes the savings along to its clients. Competition in the PBM space has heated up recently, with UnitedHealth’s OptumRX division taking deals it wouldn’t have in the past. Now the loss of 40 million scripts to Walgreens Boots took down 2017 profit growth estimates from 12% to 3% and more importantly cast a cloud over the ability for PBMs to grow profits in the future. CVS is a good stock, having grown profits every year since 2002. Management is savvy and buys back stock in addition to making smart acquisitions. In 2007 CVS acquired Caremark, a PBM that was/is growing 20% a year and in May 2015 acquired Omnicare, a PBM for seniors. One month later it purchased Target’s pharmacy business of 1600 drugstores. The recent developments have slashed CVS’s Estimated Long-Term Growth rate from 15% a year to 11%. I will sell CVS from the Growth Portfolio as the Est LTG is below the 15% I look for and I think feel this stock will be down here for a while with 2017’s profits are expected to grow just 3%. I will continue to stick with CVS in the Conservative Portfolio as this is a safe stock with a yield north of 2%. |

One Year Chart |

CVS delivered profit growth of 28% last qtr, and beat the 23% estimate, but the loss of scripts is the real news. Although 2016 profit estimates only fell 4 cents, 2017’s dropped from $6.54 to $5.96. Estimates for the next 4 qtrs are now 10%, 4%, 4% and -1%. The company does buyback stock and upped the program by an additional $15 billion after it dropped the bad news this qtr. CVS delivered profit growth of 28% last qtr, and beat the 23% estimate, but the loss of scripts is the real news. Although 2016 profit estimates only fell 4 cents, 2017’s dropped from $6.54 to $5.96. Estimates for the next 4 qtrs are now 10%, 4%, 4% and -1%. The company does buyback stock and upped the program by an additional $15 billion after it dropped the bad news this qtr. |

Fair Value |

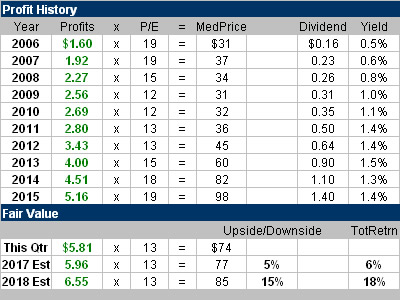

Although 2017 estimates got hammered, the company is still expected to grow profits in 2017, thus this Profit History table stays green and pretty. My Fair Value is $77 a share for 2017, which is just 5% upside. Plus you get the 2% yield. I also think CVS could come in above expectations. Although 2017 estimates got hammered, the company is still expected to grow profits in 2017, thus this Profit History table stays green and pretty. My Fair Value is $77 a share for 2017, which is just 5% upside. Plus you get the 2% yield. I also think CVS could come in above expectations. |

Bottom Line |

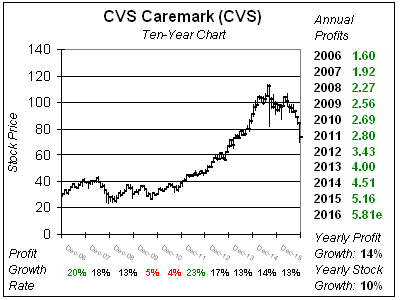

CVS has had a great history of growth, but the stock could be in for a soft period like it had in 2010 when profits grew in the mid-single digits. Notice in the Profit History table above that the stock carried a P/E of 12 then, like it does now. With profits set to slow and the Est. LTG down from 15% to 11% I will sell the stock from the Growth Portfolio. On the other hand I will continue to hold CVS in the Conservative Portfolio as this is a safe stock with a yield of 2%, a stock buyback program, and an Est. LTG in the double-digits. CVS has had a great history of growth, but the stock could be in for a soft period like it had in 2010 when profits grew in the mid-single digits. Notice in the Profit History table above that the stock carried a P/E of 12 then, like it does now. With profits set to slow and the Est. LTG down from 15% to 11% I will sell the stock from the Growth Portfolio. On the other hand I will continue to hold CVS in the Conservative Portfolio as this is a safe stock with a yield of 2%, a stock buyback program, and an Est. LTG in the double-digits. |

Power Rankings |

Growth Stock Portfolio

N/AAggressive Growth Portfolio N/AConservative Stock Portfolio 27 of 29 |