Stock (Symbol) |

Alibaba (BABA) |

Stock Price |

$168 |

Sector |

| Retail & Travel |

Data is as of |

| September 26, 2017 |

Expected to Report |

| Nov 9 |

Company Description |

Sharek’s Take |

Alibaba (BABA) got a lot of headlines after its IPO in 2014. Then the stock fell in 2015 and investors lost interest in the stock. In 2016 the stock tried to rally — and did go up some — but faded late. This year, 2017, BABA is doing fantastic. The stock has doubled year-to-date, and my indications are for the stock to continue higher. Two qtrs ago managment said 2017 revenue would grow 45-49%– well above analyst estimates of 31% growth — and I felt the stock should go materially higher on the news. Since then it has — from $140 to more than $183 recently — but I feel the stock should be more than $200. Here’s last qtr’s divisional year-over-year sales growth: Alibaba (BABA) got a lot of headlines after its IPO in 2014. Then the stock fell in 2015 and investors lost interest in the stock. In 2016 the stock tried to rally — and did go up some — but faded late. This year, 2017, BABA is doing fantastic. The stock has doubled year-to-date, and my indications are for the stock to continue higher. Two qtrs ago managment said 2017 revenue would grow 45-49%– well above analyst estimates of 31% growth — and I felt the stock should go materially higher on the news. Since then it has — from $140 to more than $183 recently — but I feel the stock should be more than $200. Here’s last qtr’s divisional year-over-year sales growth:

The company’s two main e-commerce sites are Tmall, China’s biggest business to consumer site, and Taobao, a consumer-to-consumer site like eBay. BABA also owns Youku Tudou, China’s YouTube. Management even buys back stock as well, with a $6 billion stock buyback plan in place. Profit growth just surged from 39% to 64% and looking ahead I think profits could grow an average of 50% or more for the next year. Alibaba has the size to grow and leave smaller players in the dust, and with China doing 15% of its commerce online, that means there’s lots of opportunity to capture a chunk of the remaining 85%. With excellent fundamentals and an undervalued stock, BABA is the best stock in my Power Rankings. |

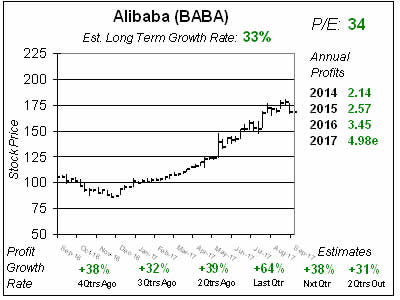

One Year Chart |

Sales grew 56% year-over-year last qtr, with profit growth ballooning to 64%, which was way above estimates of 26%. Qtrly profit estimates soared and now stand at 38%, 31%, 61% and 30%. The Est. LTG jumped from 28% last qtr to 33% this qtr. The P/E of 34 makes this stock is undervalued. Note these charts were done a couple weeks ago, and since then the stock has gone from $168 to $183. Sales grew 56% year-over-year last qtr, with profit growth ballooning to 64%, which was way above estimates of 26%. Qtrly profit estimates soared and now stand at 38%, 31%, 61% and 30%. The Est. LTG jumped from 28% last qtr to 33% this qtr. The P/E of 34 makes this stock is undervalued. Note these charts were done a couple weeks ago, and since then the stock has gone from $168 to $183. |

Fair Value |

Profit estimates surged after the company reported. 2017’s estimates jumped from $4.56 to $4.98 , 2018’s from $5.96 to $6.56 and 2019’s from $7.55 to $8.52. With the strong beat-and-raise I’m taking my Fair Value up from 3x earnings to 42x. The combination of higher profit estimates and a higher expected valuation (P/E) take my 2017 Fair Value price from $160 to $209. 2018’s Fair Value jumps from $209 to $276. Remember these charts were done a couple weeks ago when BABA was $168. Now it’s $183 and I feel even after the rise the stock’s still undervalued. Profit estimates surged after the company reported. 2017’s estimates jumped from $4.56 to $4.98 , 2018’s from $5.96 to $6.56 and 2019’s from $7.55 to $8.52. With the strong beat-and-raise I’m taking my Fair Value up from 3x earnings to 42x. The combination of higher profit estimates and a higher expected valuation (P/E) take my 2017 Fair Value price from $160 to $209. 2018’s Fair Value jumps from $209 to $276. Remember these charts were done a couple weeks ago when BABA was $168. Now it’s $183 and I feel even after the rise the stock’s still undervalued. |

Bottom Line |

Alibaba’s wasn’t a great stock after it went public, and that took investor attention away. But now the fundamentals are on fire and so is the stock. Still, even after a double so far in 2017 I think the shares have huge upside. BABA ranks 1st in the Growth Portfolio and Aggressive Growth Portfolio Power Rankings. Alibaba’s wasn’t a great stock after it went public, and that took investor attention away. But now the fundamentals are on fire and so is the stock. Still, even after a double so far in 2017 I think the shares have huge upside. BABA ranks 1st in the Growth Portfolio and Aggressive Growth Portfolio Power Rankings. |

Power Rankings |

Growth Stock Portfolio

1 of 34Aggressive Growth Portfolio 1 of 15Conservative Stock Portfolio N/A |