Stock (Symbol) |

CrowdStrike (CRWD) |

Stock Price |

$130 |

Sector |

| Technology |

Data is as of |

| March 29, 2023 |

Expected to Report |

| May 31 |

Company Description |

The Company offers Falcon platform in a SaaS subscription-based model, which delivers integrated, technologies that deliver protection and performance, while reducing customer complexity. The Company’s Falcon platform leverages a single lightweight-agent architecture with integrated cloud modules spanning multiple security markets, including corporate workload security, managed security services, security and vulnerability management, information technology (IT) operations management, threat intelligence services, identity protection and log management. It also offers approximately 22 cloud modules on its Falcon platform, which include Falcon Prevent, Falcon Insight, Falcon Device Control, Falcon Firewall Management, Falcon XDR, Falcon Discover, Falcon Spotlight and others. Source: Refinitiv |

Sharek’s Take |

Crowdstrike (CRWD) stock seems to have bottomed after falling from almost $300 down to below $100. The stock was getting a lot of negative news around the beginning of the year that business was bad. Meanwhile, insiders were buying the dip. And in the end, the company was doing fine and the stock has recently gone back up to $130. Last quarter, CRWD added a record number of new customers, and had strong expansion within its current customer base (aka “land and expand”). After earnings, the stock rose after the company beat the street and increased next quarter’s profit estimates as well as 2023 profit estimates. The company saw strong growth in enterprice, non-enterprice, and public sector accounts. Still, revenue gowht has slowed during the past our quarters, from 61% to 58%, 53% and most recently 48%. Crowdstrike (CRWD) stock seems to have bottomed after falling from almost $300 down to below $100. The stock was getting a lot of negative news around the beginning of the year that business was bad. Meanwhile, insiders were buying the dip. And in the end, the company was doing fine and the stock has recently gone back up to $130. Last quarter, CRWD added a record number of new customers, and had strong expansion within its current customer base (aka “land and expand”). After earnings, the stock rose after the company beat the street and increased next quarter’s profit estimates as well as 2023 profit estimates. The company saw strong growth in enterprice, non-enterprice, and public sector accounts. Still, revenue gowht has slowed during the past our quarters, from 61% to 58%, 53% and most recently 48%.

CrowdStrike is one of the world’s largest cybersecurity companies, serving 556 of the Global 2000, 271 of the Fortune 500, and 15 of the top US banks as of January 21, 2023. The company provices is a crowd-sourced security, which is software that learns from cyber attacks. The company has a threat intel platform that is spying on customer traffic. When one customer gets hit by an attempted cyber attack, CRWD sees this first attack and can strike the threat for all its customers. CRWD is about endpoint protection for PCs, laptops, iPads and mobile phones. This is defending the hardware at the end of the internet, like when Norton made famous with PC protection. On the other hand, Zscaler protects the traffic that flows. CRWD recently acquired Preempt Security and Humio. These new acquisitions put the company in two new arenas for growth: zero-trust security and data analysis. CRWD’s products are modules that can be packaged or bought separately:

Here are some of the important business highlights from last qtr:

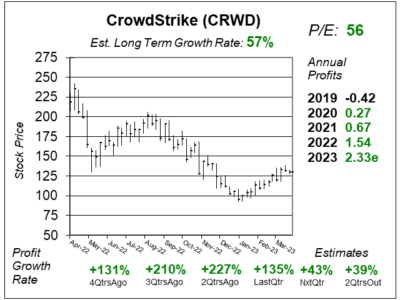

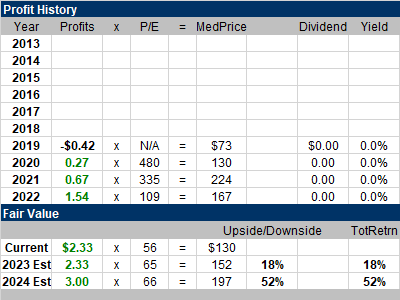

CRWD is one of the fastest growing publicly-traded companies with great growth opportunity ahead. CRWD was the second fastest cloud-native software as a service company (SaaS) to reach over $2 billion in Annual Recurring Revenue (ARR), behind Zoom (ZI). The Estimated Long-Term Growth Rate of 57% is one of the highest in the market. And this company is profitable. CRWD is delivering cash flow, and management expects free cash flow margin to be 30% of revenue in 2023. CRWD is part of the Aggressive Growth Portfolio. Last quarter I wrote” I want to add it to the Growth Portfolio after the stock bottoms and turns higher.” but the shares are up from $100 to $130 since then. So I missed buying low. I think the stock is worth $152 so there’s still upside, but I won’t add CRWD to the Growth Portfolio yet as companies are trying to reduce software spend with the economy pulling back. |

One Year Chart |

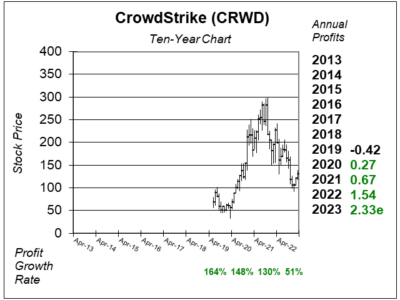

This stock has come up nicely from its lows. This stock has come up nicely from its lows.

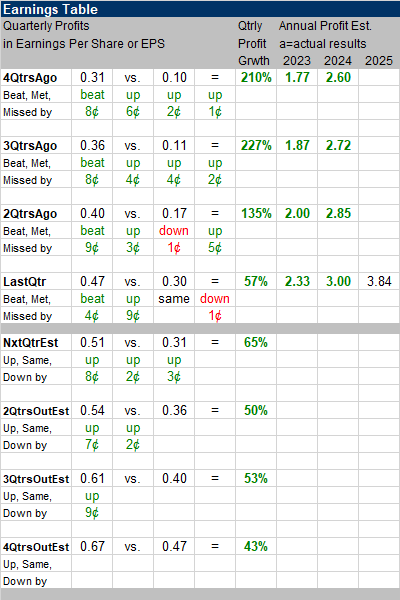

The Est. LTG of 57% is very impressive, but that figure is down from 59% last qtr. The P/E of 56 is good. The P/E was 50 last qtr. Quarterly profit growth has been excellent! Estimates for the next two quarters are solid too. Notice CRWD’s Annual Profits. Record profits each year and nice growth rates as well. |

Earnings Table |

Last qtr, CrowdStrike posted 57% profit growth and beat expectations of 43% growth. Revenue increased 48%, year-over-year. Free cash flow was 33% of revenue. Here are the geographical results during the qtr: Last qtr, CrowdStrike posted 57% profit growth and beat expectations of 43% growth. Revenue increased 48%, year-over-year. Free cash flow was 33% of revenue. Here are the geographical results during the qtr:

Revenue growth was delivered by strong product expansions within existing customers and new customer additions from large enterprise, non-enterprise, and government sector accounts. Within small and medium businesses, they saw strong initial success in the Falcon Go bundle as this was designed as a starter package for smaller businesses for a lower price. Management indicated that they did not see any kind of budget tightening from their customers as they prioritize the cybersecurity of their businesses. That’s the opposite of what they said last quarter. Annual Profit Estimates have increased every quarter since I started covering the company in 2020 Q4. For Fiscal 2024, management expects revenue to grow 32% to 35%. Qtrly Profit Estimates are for 65%, 50%, 53%, and 43% profit growth the next 4 qtrs. For next qtr, management projects revenue to grow 38% to 39%, in line with analysts’ estimates of 39%. |

Fair Value |

The stock sells for 10x 2023 revenue estimates this qtr. My Fair Value is 12x revenue estimates. So the stock seems undervalued here. Also, last quarter, my Fair Values were $152 and $197, exactly the same as we have now. Upside is very good when we look to 2024. The stock sells for 10x 2023 revenue estimates this qtr. My Fair Value is 12x revenue estimates. So the stock seems undervalued here. Also, last quarter, my Fair Values were $152 and $197, exactly the same as we have now. Upside is very good when we look to 2024.

Current: 2023 Est: 2024 Est: |

Bottom Line |

CrowdStrike (CRWD) stock has had a volatile history, and the stock is still well off its highs from last year. When I look back to my CRWD 2021 Q3 research report when the shares were $271, the stock sold for 43x 2021 revenue estimates. In retrospect, forty-three times revenue was too much. CrowdStrike (CRWD) stock has had a volatile history, and the stock is still well off its highs from last year. When I look back to my CRWD 2021 Q3 research report when the shares were $271, the stock sold for 43x 2021 revenue estimates. In retrospect, forty-three times revenue was too much.

Cybersecurity is proving to be an expense that companies have to absorb, even in the face of a recession. Although CRWD’s growth is slowing, these numbers still impressed me. CRWD stays at 7th in the Aggressive Growth Portfolio Power Rankings. The stock will be purchased for the Growth Portfolio on Monday and rank 14th in the Power Rankings. |

Power Rankings |

Growth Stock Portfolio

14 of 27Aggressive Growth Portfolio 7 of 20Conservative Stock Portfolio N/A |