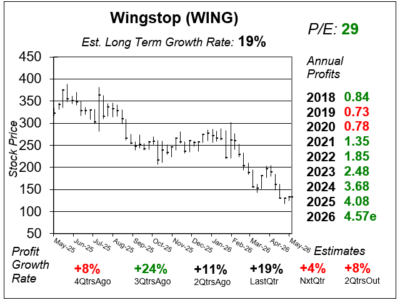

Wingstop (WING) Stock Suffers as Same Store Sales Declined 9% Last Quarter

Wingstop (WING) stock has been free falling as same store sales have been declining. But with a P/E of just 29, WING has good upside.

Wingstop (WING) stock has been free falling as same store sales have been declining. But with a P/E of just 29, WING has good upside.

Wingstop (WING) stock just lost half its value in the past year. I think this quick-service chicken shop is a good investment here.

Wingstop (WING) same store sales were down 6% last quarter, but management is cooking up some good things for 2026.

Wingstop (WING) has delivered poor results the past two quarters, but the story is still positive when we look at WING’s potential.

Wingstop (WING) fell earlier this year on anticipation of slowing same store sales (SSS). But WING stock rose when results came in.

Wingstop (WING) stock recently went from $200 to $400, then back down to $225. Here’s why 2025 is a good time to buy WING.

Wingstop (WING) stock had a big run higher, and is now digesting past gains. Here’s why the stock is at a good buy point now.

Wingstop (WING) is growing rapidly as revenue jumped 45% last quarter as same store sales increased a solid 29% year-over-year.

Wingstop (WING) delivered profit growht of 66% last qtr — triple the 22% expected — as sales surged 37% from a year ago.

Wingstop (WING) has impressed investors with its robost same store sales growth, which clocked in at 21% last quarter in the US.

Wingstop (WING) delivered blowout results last quarter as profits soared 53% and beat estimates of 13%.

Wingstop (WING) sees deliveries on the rise. Perhaps from 30% of sales to greater than 50%. And that’s increasing unit volume too.

The Wingstop (WING) is expanding as ads helped to drive revenue up 43% last qtr while profits surged 74% due to lower wing prices.

Wingstop (WING) delivered excellent results last qtr — 150% profit growth on 46% revenue growth — as wing prices fell 49%.

Wingstop (WING) had profits surge last qtr as chicken wing prices fell. In addition, its new Chicken Sanwich is a catalyst for the stock.

Wingstop (WING) might have a catalyst coming in September when it launches its chicken sandwich, tossed in a choice of 12 sauces.

Wingstop (WING) stock is down while the company is benefiting from lower wing prices. And 52 is a good P/E to buy in at.

Wingstop’s (WING) chicken prices have been coming down, and that might mean better profitability in the upcoming quarters.

Wingstop (WING) is trying to grow from around 1700 locations to 6000. Expansion into Manhattan, England and Canada helps.

YES! Wingstop (WING) plans to open 25 company owned locations in Manhattan, with half of them ghost kitchens. Mmmm!

Wingstop (WING) is selling a lot more food these days, especially via digital orders. But high wing prices could cut profits.

Wingstop (WING) often has a high P/E as the company has big plans for expanding from 1500 locations to 6000-plus.

Wingstop (WING) could have a catalyst on its hands with bone-in thighs, which would come in 11 bold distinctive flavors.

Wingstop (WING) has some fantastic numbers. But that’s COVID related. What I really like is the opportunity in Europe.

Wingstop (WING) has been rolling as its digital sales have jumped from 40% of sales to 65% since the Coronavirus outbreak.

Wingstop (WING) is in a perfect position for future growth as pick-up and delivery is big in a Coronavirus world.

Wingstop (WING) has lots going right including delivery with DoorDash. What it doesn’t have is a reasonable price.

Wingstop’s (WING) P/E is 131 even though profit growth is expected to be -12% this year. WING seems too expensive every qtr.

Wingstop (WING) has a 101 P/E. Wow! And profits are expected to decline in 2019. There’s more to the story here: Dividends.

Wingstop (WING) is one of the fastest growing restaurants around, but the stock’s P/E of 73 is out-of-whack — and profit growth looks weak.

Investors are valuing Wingstop (WING) stock on the growth opportunity the company has, both in the U.S. and Internationally. I think a 27 P/E for 22% growth is high.

Wingstop (WING) has vast growth opportunity. But WING is growing profits in the teens and has a P/E of 63. The stock seems high.

Shares of Wingstop (WING) are on fire, but with a P/E of 57 the numbers have to be as well. Let’s take a look at one of the tastiest restaurant stocks around.

WIngstop (WING) is a new “hot stock” in the stock market. Here’s our first take on what we think the stock is really worth.