Stock (Symbol) |

MasterCard (MA) |

Stock Price |

$596 |

Sector |

| Financial |

Data is as of |

| September 4, 2025 |

Expected to Report |

| October 29 |

Company Description |

The Company allows user to make payments by creating a range of payment solutions and services using its brands, which include MasterCard, Maestro and Cirrus. It provides a range of products and solutions that support payment products, which customers can offer to their cardholders. The Company’s services facilitate transactions on its core network among account holders, merchants, financial institutions, businesses, governments and other organizations in markets globally. Its products include consumer credit, consumer debit, prepaid and commercial credit and debit. It also provides integrated offerings such as cyber and intelligence products, information and analytics services, identity verification services, consulting, loyalty and reward programs, processing and open banking. Source: Refinitiv |

Sharek’s Take |

MasterCard (MA) continues to be that high-teens grower it usually is, as last quarter the company delivered 16% profit growth on 17% revenue growth. Management said consumer spending is still healthy because unemployment is low and wages are rising faster than inflation. This trend is seen in both wealthy and average consumers. Although there are uncertainties from government policies and global tensions, MasterCard management is optimistic since the main factors driving spending remain solid. MasterCard (MA) continues to be that high-teens grower it usually is, as last quarter the company delivered 16% profit growth on 17% revenue growth. Management said consumer spending is still healthy because unemployment is low and wages are rising faster than inflation. This trend is seen in both wealthy and average consumers. Although there are uncertainties from government policies and global tensions, MasterCard management is optimistic since the main factors driving spending remain solid.

MasterCard is a technology company in the global payments industry that connects consumers, financial institutions, merchants, governments, digital partners, businesses and other organizations worldwide, enabling them to use electronic forms of payment instead of cash and checks (source: 2019 Annual Report). It links the account holder, the account holder’s bank, the merchant, and the merchant’s bank. The company derives revenue based on fees for gross dollar volume (GDV) purchases. Last December MA acquired Recorded Future, a provider of cybersecurity including AI-driven threat intelligence capabilities, identity solutions, and real-time fraud scoring. The company’s operating categories:

MasterCard is a safe stock with high certainty and consistency that I think might give investors mid-to-high teens returns long-term. MA currently has an Estimated Long-Term Growth Rate of 15% a year and a dividend yield of less than 1%. Management buys back billions in stock and pays a dividend that’s increased every year since 2012. In Fiscal 2024, management repurchased $11 billion in stock and paid $2.4 billion in dividends. MA is part of the Conservative Portfolio and Growth Portfolio. |

One Year Chart |

MA stock has been a warrior lately. But now I feel the shares are a tad overvalued. MA stock has been a warrior lately. But now I feel the shares are a tad overvalued.

This quarter, the P/E is 36. My Fair Value is a P/E of 35. The P/E was 37 last quarter. The Est. LTG of 15% is around where I think it should be. This figure is the same as last qtr. Qtrly profit growth is not consistent, as the company gives rebates when it signs new customers. Estimates are for slowing growth ahead, but MA has been beating the street, so I expect that to continue. |

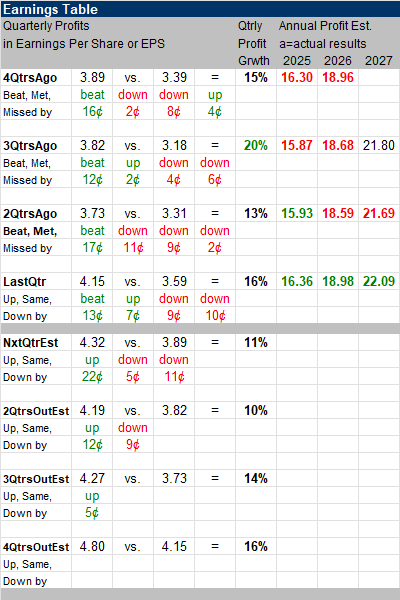

Earnings Table |

Last qtr, MasterCard delivered 16% profit growth and beat estimates of 12%. Revenue increased 17%, year-over-year, versus estimates of 14%. Last qtr, MasterCard delivered 16% profit growth and beat estimates of 12%. Revenue increased 17%, year-over-year, versus estimates of 14%.

Revenue growth was driven by healthy customer spending and a 15% rise in cross-border volumes. Gross Dollar Volume (GDV) grew 9%, with US GDV increasing 6% (credit up 6%, debit up 7%) and International volumes rose 10% (credit up 9%, debit up 11%). Rebates and incentives rose 17% as MasterCard signed new and renewed deals. Annual Profit Estimates are all up this qtr. Qtrly Profit Estimates are for 11%, 10%, 14%, and 16% growth the next 4 qtrs. Analysts think MA revenue will grow 16% next qtr. |

Fair Value |

My Fair Value P/E is 35. The stock currently has a 36P/E. My Fair Value P/E is 35. The stock currently has a 36P/E.

MA is 4% above my Fair Value price of $573. Note the 44 and 42 P/Es the stock had in 2020 and 2021. Those figures were too high. So the stock had to digest some gains in 2022 and 2023 as it went sideways (you can see this in the ten-year chart below). |

Bottom Line |

MasterCard (MA) stock has a lot of great traits, including a double-digit growth rate, a rising dividend, a stock buyback program and a stable business that churns out growth. MasterCard (MA) stock has a lot of great traits, including a double-digit growth rate, a rising dividend, a stock buyback program and a stable business that churns out growth.

Notice in this chart profit growth has been 17% a year this past decade. That’s consistent high-teens growth. But the stock’s grown 20% a year, suggesting to me the stock’s gotten ahead of itself. This is true, as MA is a little above its Fair Value. MA movesfrom 12th to 13th in the Conservative Growth Portfolio Power Rankings. The stock ranks 31st of 32 stocks in the Growth Portfolio Power Rankings. |

Power Rankings |

Growth Stock Portfolio

31 of 32Aggressive Growth Portfolio N/AConservative Growth Portfolio 13 of 19 |