Stock (Symbol) |

Costco (COST) |

Stock Price |

$855 |

Sector |

| Food & Necessities |

Data is as of |

| January 2, 2026 |

Expected to Report |

| March 4 |

Company Description |

The Company operates an international chain of membership warehouses, mainly under the Costco Wholesale name. The Company’s warehouses are designed to help small- to medium-sized businesses reduce costs in purchasing for resale and for everyday business use. The Company offers merchandise in various categories, which include groceries, candy, appliances, television and media, automotive supplies, tires, toys, hardware, sporting goods, jewelry, watches, cameras, books, housewares, apparel, health and beauty aids, furniture, office supplies and office equipment. Members can also shop for private label Kirkland Signature products. It operates approximately 923 warehouses worldwide. It also operates self-service gasoline stations. The Company operates e-commerce websites in the United States, Canada, Mexico, United Kingdom, Korea, Taiwan, Japan, and Australia. Source: Refinitiv |

Sharek’s Take |

Costco’s (COST) growth last quarter has continued to be driven by its e-commerce division and membership strength. Digitally enabled comparable sales posted a strong growth of 21% last quarter, supported by continued web and app improvements, with site traffic up 24% and app traffic up 48%. In the earnings call, management highlighted same-day delivery, via Instacart in the US and Uber Eats/DoorDash internationally, outpaced overall digital sales. New personalization features boosted product recommendations, while AI-driven pharmacy inventory management improved in-stock rates to over 98%, driving mid-teen growth in prescriptions filled. Meanwhile, Costco’s membership fee income rose 14% year over year, with high renewal rates. Overall, COST recorded 11% profit growth on 8% increase in revenue last quarter. Both numbers are in-line with the stock’s long-term growth rates. Costco’s (COST) growth last quarter has continued to be driven by its e-commerce division and membership strength. Digitally enabled comparable sales posted a strong growth of 21% last quarter, supported by continued web and app improvements, with site traffic up 24% and app traffic up 48%. In the earnings call, management highlighted same-day delivery, via Instacart in the US and Uber Eats/DoorDash internationally, outpaced overall digital sales. New personalization features boosted product recommendations, while AI-driven pharmacy inventory management improved in-stock rates to over 98%, driving mid-teen growth in prescriptions filled. Meanwhile, Costco’s membership fee income rose 14% year over year, with high renewal rates. Overall, COST recorded 11% profit growth on 8% increase in revenue last quarter. Both numbers are in-line with the stock’s long-term growth rates.

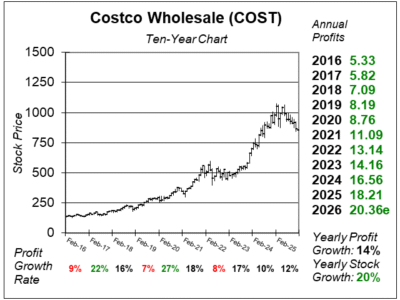

Costco is the 2nd largest global retailer with more than 130 million members. The company began operations in 1983 in Seattle, Washington. In 1993, the company merged with Price Club, which pioneered the membership warehouse concept in 1976 (and was a hot stock during its early years). It ended Fiscal 2025 with 914 locations worldwide, including 629 in the US or 69% and 31% Internationally (Canada, Mexico, Japan, the United Kingdom, Korea, Australia, Taiwan, China, Spain, France, Sweden, Iceland and New Zealand). The company opens around 20 to 30 locations annually. Costco also runs e-commerce websites in the United States, Canada, United Kingdom, Mexico, South Korea, Taiwan, Japan, and Australia. The profit Costco makes is mostly made up of the annual membership fees it brings in. In Fiscal 2025, COST had retail sales of $269.9 billion, membership fees of $5.3 billion, and net income of $8.1 billion. Here are some stats from the last qtr:

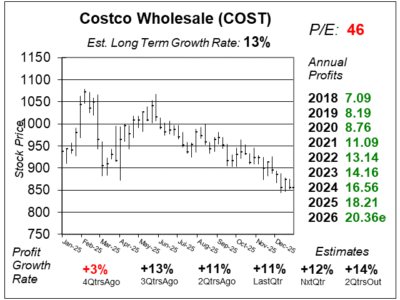

Costco is one of the world’s safest stocks, but it’s basically a 10% to 12% grower with a lofty P/E. Analysts give the stock an Estimated Long Term Growth Rate (Est. LTG) of 13% per year and the stock yields around 1% per year. Management buys back stock, pays a quarterly dividend, and has also paid occasional one-time dividends. The big issue with this stock is its expensive. I sold Costco from the Conservative Growth Portfolio in January 2024 because I felt P/E was too high at 41. This quarter it’s 46. So COST is on the radar and if the stock drops some more, I’ll likely buy in. |

One Year Chart |

Costco stock has declined from ~$1000 to ~$850 the past few qtrs. But the stock still isn’t cheap enough to buy. Costco stock has declined from ~$1000 to ~$850 the past few qtrs. But the stock still isn’t cheap enough to buy.

The P/E of 46 is high. My Fair Value is a 37 P/E. I think the stock is worth $753. It’s $855 this qtr. The Est. LTG was 9% last quarter and is 13% this quarter. Nice! Profit growth has been 11% the past two quarters, and its expected to accelerate to 12% and 14% the next 2 qrts. |

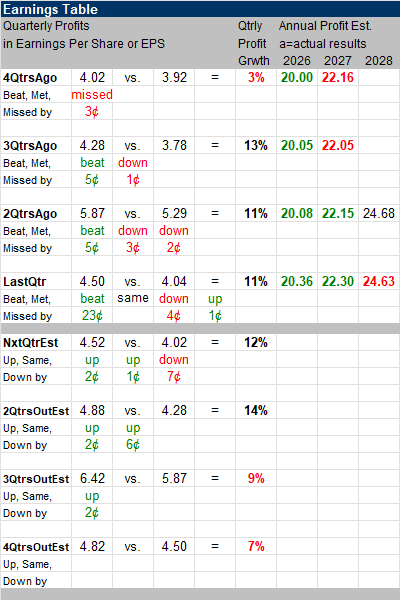

Earnings Table |

Last quarter, Costco delivered 11% profit growth and beat estimates of 6%. Revenue increased 8%, year-on-year and met estimates of 8%. Same-store sales increased 6% including 6% in the US, 9% in Canada and 7% in other International markets. Traffic and average transaction size both increased 3% globally. Membership fee income grew 14% year over year. Last quarter, Costco delivered 11% profit growth and beat estimates of 6%. Revenue increased 8%, year-on-year and met estimates of 8%. Same-store sales increased 6% including 6% in the US, 9% in Canada and 7% in other International markets. Traffic and average transaction size both increased 3% globally. Membership fee income grew 14% year over year.

Annual Profit Estimates increased somewhat. Qtrly Profit Estimates are 12%, 14%, and 9% and 7% for the next 4 qtrs. Analysts believe COST revenue will grow by 8% next quarter. |

Fair Value |

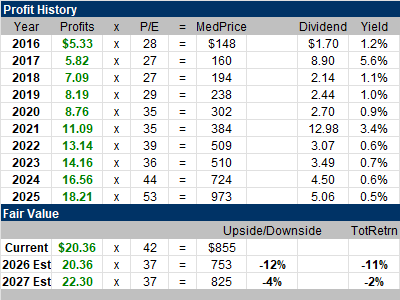

Costco’s P/E had risen steadily during the past decade. I think the P/E is too high now. Costco’s P/E had risen steadily during the past decade. I think the P/E is too high now.

The stock has a 46 P/E this qtr, and my Fair Value P/E is 37. At the current price of $855, and a Fair Value of $753 a share, the stock is 12% overvalued in my opinion. The company has a Fiscal Year end on August 31. |

Bottom Line |

Costco (COST) is a quality Blue Chip stock with high certainty, a stock buyback program, qtrly dividends and a history of big surprise dividends. This has been a steady winner for many decades, thus investors really appreciate the stock. Costco (COST) is a quality Blue Chip stock with high certainty, a stock buyback program, qtrly dividends and a history of big surprise dividends. This has been a steady winner for many decades, thus investors really appreciate the stock.

Costco needs to continue to digest its prior gains. The stock still seems too high in my opinion. COST is on the radar for the Conservative Portfolio. |

Power Rankings |

Growth Stock Portfolio

N/AAggressive Growth Portfolio N/AConservative Stock Portfolio N/A |