Stock (Symbol) |

American Express (AXP) |

Stock Price |

$314 |

Sector |

| Financial |

Data is as of |

| April 25, 2026 |

Expected to Report |

| July 24 |

Company Description |

The Company provides its customers with access to products, insights, and experiences that builds business. It operates under four segments: U.S. Consumer Services (USCS), Commercial Services (CS), International Card Services (ICS), and Global Merchant and Network Services (GMNS). USCS offers travel and lifestyle services as well as banking and non-card financing products. CS offers payment and expense management, banking and non-card financing products. CS also issues corporate cards and provides services to select global corporate clients. ICS also provides services to international customers, including travel and lifestyle services, and manages certain international joint ventures and its loyalty coalition businesses. GMNS provides multi-channel marketing programs and capabilities, services and data analytics. It provides credit and charge cards to consumers, small businesses, mid-sized companies and corporations. |

Sharek’s Take |

Last quarter, American Express (AXP) reported solid performance with 18% profit growth on 11% revenue growth. Growth was driven by higher card member spending from premium, Millennial and Gen Z customers. This contributed to cardmember spending of 10%, the highest quarterly growth in 3 years, with retail spending up 11% year on year (YoY) and luxury retail spending up 18% YoY. Meanwhile, demand for fee-based premium products remained strong, driving a 16% growth in net card fees. Management also highlighted ongoing investments in AI to enhance customer engagement and deliver more personalized experiences. The company recently introduced Amex Agentic Commerce Experiences and Amex Agent Purchase Protection, leveraging AI agents to automate shopping interactions. Last quarter, American Express (AXP) reported solid performance with 18% profit growth on 11% revenue growth. Growth was driven by higher card member spending from premium, Millennial and Gen Z customers. This contributed to cardmember spending of 10%, the highest quarterly growth in 3 years, with retail spending up 11% year on year (YoY) and luxury retail spending up 18% YoY. Meanwhile, demand for fee-based premium products remained strong, driving a 16% growth in net card fees. Management also highlighted ongoing investments in AI to enhance customer engagement and deliver more personalized experiences. The company recently introduced Amex Agentic Commerce Experiences and Amex Agent Purchase Protection, leveraging AI agents to automate shopping interactions.

American Express is a globally integrated payments company in providing credit and charge cards to individuals and businesses with high credit scores. The company is both a card issuer (like Chase and Citi are) and a card network (like MasterCard and Visa). American Express’ integrated payments platform has direct relationships with Merchants and Card Members, creating a closed loop so the company has direct access to information. American Express can analyze information on spending to underwrite risk, reduce fraud and do targeted marketing. What makes American Express special is its Membership Rewards program, which include benefits such as airport lounge access, dining experiences, and other travel benefits. The company has been attracting younger, Millennial and Gen Z customers. Amex’s Platinum Card has evolved into a premium lifestyle card with a wide range of benefits that appeal cross generations. Here’s a short history of American Express:

AXP engages in businesses comprising four operating segments:

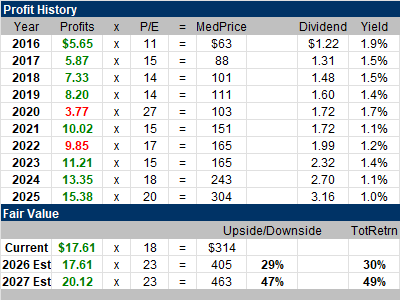

American Express is a reasonably safe stock that is part of the Dow Jones Industrial Average. Amex does have some credit risk, as the company holds credit card loans, unlike Visa and MasterCard. There have been years during the past decade when profits haven’t hit All-Time highs. Thus, this stock doesn’t have the great certainty that MasterCard and Visa possess. In 2025, AXP returned $7.6 billion of capital to its shareholders, including $2.3 billion of dividends and $5.3 billion of share repurchases. I used to consider this a ten percent grower (Est. LTG + yield) long term, but now management aspirations are mid-teens profit growth. AXP is part of the Conservative Portfolio. With a P/E of 18, this stock has room to move higher. |

One Year Chart |

AXP stock has been solid. The shares just digested some gains during a recent market correction. THis looks like a good time to buy. AXP stock has been solid. The shares just digested some gains during a recent market correction. THis looks like a good time to buy.

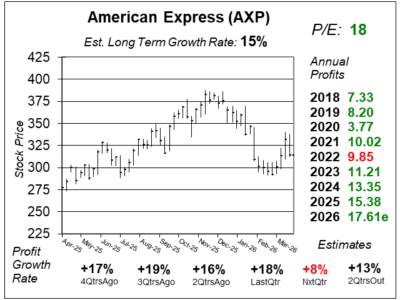

The P/E of 18 is in green, signifying the stock is good value. My fair value is P/E of 23. Analysts have an Est. LTG of 15% on this stock, same with last quarter. Quarterly profit growth was a solid 18% last quarter and is expected to ease to 8%. But AXP beat the street by 29 cents last qtr, and if it beats by the same amount this qtr that could be 29% growth. |

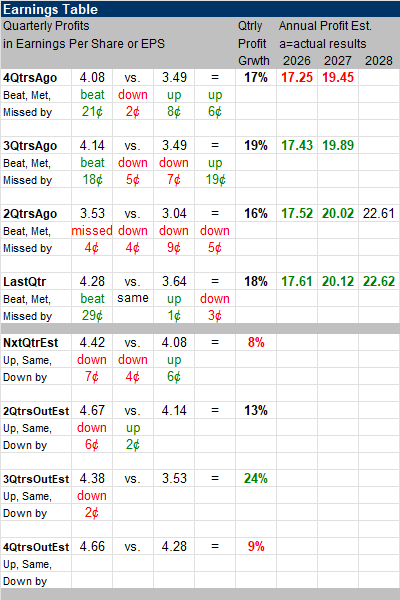

Earnings Table |

Last quarter, American Express delivered 18% profit growth and beat estimates of 10% growth. Revenue increased 11%, which was slightly above analyst expectations of 10%. Last quarter, American Express delivered 18% profit growth and beat estimates of 10% growth. Revenue increased 11%, which was slightly above analyst expectations of 10%.

Segment revenue growth was:

Annual Profit Estimates increased this quarter. For 2026, management expect revenue growth to be 9-10% YoY. Quartely Profit Estimates for the next 4 quarters are 8%, 13%, 24%, and 9% growth. Analysts estimate AXP’s revenue will grow 10% next quarter. |

Fair Value |

This quarter, the stock is $314, giving it a P/E of 18. This quarter, the stock is $314, giving it a P/E of 18.

My Fair Value is a P/E of 23, and that equates to $405 a share, 29% higher than the recent quote. Based on 2027 estimates, the stock has an upside of 47%, which would be ample returns for a conservative stock.

|

Bottom Line |

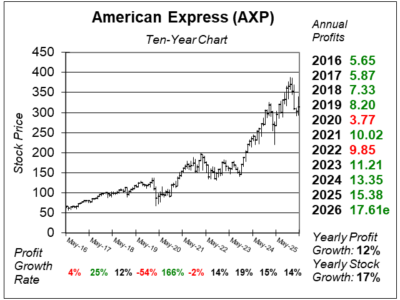

American Express (AXP) has had an erratic profit history. Also, the stock hasn’t been a steady grower the past decade. But notice below the chart that profit growth has been solid the past four years. American Express (AXP) has had an erratic profit history. Also, the stock hasn’t been a steady grower the past decade. But notice below the chart that profit growth has been solid the past four years.

American Express is a nice card to have with perks younger consumers like. With the US economy humming along, this company should continue to do well. And the recent dip gives new investors a buying opportunity. AXP moves from 8th to 7th in the Conservative Growth Portfolio Power Rankings. |

Power Rankings |

Growth Stock Portfolio

N/AAggressive Growth Portfolio N/AConservative Growth Portfolio 7 of 19 |