Stock (Symbol) |

Amphenol (APH) |

Stock Price |

$141 |

Sector |

| Industrials & Energy |

Data is as of |

| May 4, 2026 |

Expected to Report |

| July 29 |

Company Description |

The Company operates through three segments: The Harsh Environment Solutions segment designs, manufactures and markets a range of ruggedized interconnect products and other products for use in the industrial, defense, commercial aerospace, automotive, mobile networks, medical and other markets. Communications Solutions segment designs, manufactures and markets a range of connector and interconnect systems for use in the information technology and data communications, mobile devices, industrial, mobile networks, broadband communications, automotive, commercial aerospace and defense end markets. Its Interconnect and Sensor Systems segment designs, manufactures and markets a range of sensors, sensor-based systems, connectors and value-add interconnect systems. Source: Refinitiv |

Sharek’s Take |

Connector manufacturer Amphenol (APH) is one of the biggest behind-the-scenes winners of the AI infrastructure boom, supplying the high-speed cables, power systems, and fiber connections used inside advanced AI servers and data centers. APH’s Communications Solutions division makes cables and connectors, and saw sales growth of 88% last quarter. Management stated AI-related demand was the main reason order volume grew 78% year-over-year, with customers continuing to expand AI data center capacity at a rapid pace. Management also discussed working on next-generation AI data center architectures, including optical networking and co-packed optics (CPO), which are newer technologies designed to move AI data faster with lower power usage. Customers are demanding more bandwidth, higher speeds, and denser interconnect systems for future AI clusters. Amphenol believes its broader product lineup positions it well to capture that demand. Connector manufacturer Amphenol (APH) is one of the biggest behind-the-scenes winners of the AI infrastructure boom, supplying the high-speed cables, power systems, and fiber connections used inside advanced AI servers and data centers. APH’s Communications Solutions division makes cables and connectors, and saw sales growth of 88% last quarter. Management stated AI-related demand was the main reason order volume grew 78% year-over-year, with customers continuing to expand AI data center capacity at a rapid pace. Management also discussed working on next-generation AI data center architectures, including optical networking and co-packed optics (CPO), which are newer technologies designed to move AI data faster with lower power usage. Customers are demanding more bandwidth, higher speeds, and denser interconnect systems for future AI clusters. Amphenol believes its broader product lineup positions it well to capture that demand.

Founded in 1925 in Sidney, New York, Amphenol is a leader in military, aerospace, and networking connector manufacturer. Originally, the company specialized in magnetos for aviation. A magneto is an electrical generator that uses magnets to produce electric current for airplanes. Eventually, engineers then developed ignition systems for lawnmowers, washing machines, and the largest aircraft engines. In the 1950s, the company branched out into electrical connectors. Today, Amphenol has manufacturing operations in 40 countries worldwide. The company grows both organically and via acquisitions. The company recently acquired:

Amphenol has three operating segments:

End markets include (with last qtr’s stats):

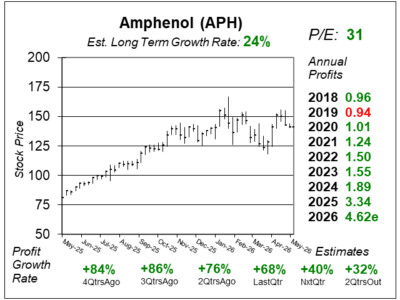

APH is a safe stock that’s recorded record profits (EPS) in 21 of the past 23 years (except 2009 and 2019). Dividends have grown each year since 2011. The stock has an Estimated Long Term Growth Rate of 24% per year and the dividend yield is 1%. In 2025, management spent $1.5 billion on stock buybacks and dividends. The dividend was raised 52% in 2025. Amphenol is in a sweet spot right now. And with a P/E of just 31, I think the stock has further upside. APH is part of the Conservative Growth Portfolio, Growth Portfolio, and Focus List. Robotics are the next frontier. |

One Year Chart |

APH stock has been building a base as it digests a recent run from $75 to $150. I bought this stock on May 2, 2025 at $81 when it broke out to a new All-Time high. APH has since become a leader within the AI stock collection. APH stock has been building a base as it digests a recent run from $75 to $150. I bought this stock on May 2, 2025 at $81 when it broke out to a new All-Time high. APH has since become a leader within the AI stock collection.

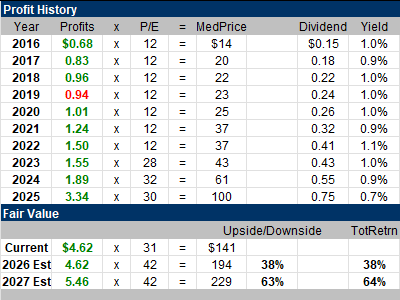

The P/E is 31. I feel the P/E can get up to 42. More on this later. The Estimated Long-Term Growth Rate (Est. LTG) is 24%, up from 22% last qtr. Qtrly profit growth has been excellent. |

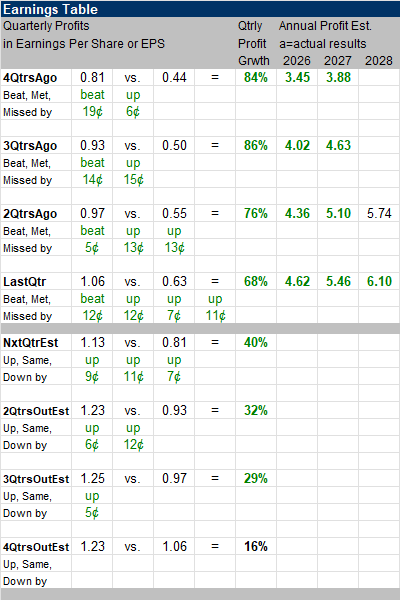

Earnings Table |

Last qtr, APH reported 68% profit growth and whipped analyst estimates of 48%. Revenue increased by 58% versus estimates of 46%. Note profits have increased for 8 consecutive quarters (from $0.44 to $1.06). Operating Margin was 27.3%, up from 23.5% a year ago. Here are some highlights from the Earnings Call: Last qtr, APH reported 68% profit growth and whipped analyst estimates of 48%. Revenue increased by 58% versus estimates of 46%. Note profits have increased for 8 consecutive quarters (from $0.44 to $1.06). Operating Margin was 27.3%, up from 23.5% a year ago. Here are some highlights from the Earnings Call:

Annual Profit Estimates have been trending higher. Lots of green in this Earnings Table! Quarterly profit Estimates are 40%, 32%, 29%, and 16% for the next 4 qtrs. Analysts think revenue will grow a solid 42% next quarter. |

Fair Value |

APH had a P/E of just 12 a decade ago as it was considered to be a slow-growing industrial stock. Now the stock is getting more respect, and the P/E is higher. APH had a P/E of just 12 a decade ago as it was considered to be a slow-growing industrial stock. Now the stock is getting more respect, and the P/E is higher.

At $141 a share, APH has a P/E of 31 this qtr. My Fair Value is a P/E of 42, which equates to $194 in 2026, 38% above the recent quote. 2027 Fair Value sits at $229 a share, giving the stock upside of 63% in my opinion. |

Bottom Line |

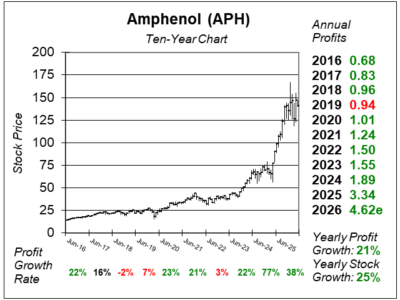

Amphenol (APH) has a beautiful ten-year chart. In fact, the 20 year view looks good as well. Notice profit growth really accelerated in 2021, around the time the stock broke out and went on a nice run higher. But the stock has been on a sharp rise recently. Amphenol (APH) has a beautiful ten-year chart. In fact, the 20 year view looks good as well. Notice profit growth really accelerated in 2021, around the time the stock broke out and went on a nice run higher. But the stock has been on a sharp rise recently.

The revolution in AI is a unique opportunity for Amphenol. Its products are critical components in next generation networks. Defense is cooking as well. I assume more space flights will require more Amphenol products. Next up: robotics. APH ranks 5th in the Growth Portfolio and Focus List Power Rankings. APH ranks 3rd in in the Conservative Growth Portfolio Power Rankings. |

Power Rankings |

Growth Stock Portfolio

5 of 29Focus List 5 of 17Conservative Stock Portfolio 3 of 19 |