Stock (Symbol) |

Palantir (PLTR) |

Stock Price |

$24 |

Sector |

| Technology |

Data is as of |

| March 5, 2024 |

Expected to Report |

| May 6 |

Company Description |

The Company’s three principal software platforms include Palantir Gotham (Gotham), Palantir Foundry (Foundry), and Palantir Apollo (Apollo). Gotham enables users to identify patterns hidden deep within datasets, ranging from signals intelligence sources to reports from confidential informants. It also facilitates the hand-off between analysts and operational users, helping operators plan and execute real-world responses to threats. Foundry transforms the ways organizations operate by creating a central operating system for their data. Apollo is a cloud-agnostic, single control layer that coordinates ongoing delivery of new features, security updates, and platform configurations, helping to ensure the continuous operation of critical systems and allowing its customers to run their software in virtually any environment. Source: Refinitiv. |

Sharek’s Take |

Palantir (PLTR) delivered a blockbuster quarter with its commercial business here in America. Last quarter US Commercial revenue spiked 70% year-over-year as customer count jumped 55% from a year ago. And business is bound to get better as US Commercial Total Contact Velue (TCV) lept 107%. What caused this spike? Palantir’s AIP Bootcamps, a 5 day bootcamp for the company to understand (1) how to apply AI to its operations (2) develop use casses and (3) onboard and train users. The company has already done 560 bootcamps with 465 organizations just this year. Management has never seen this level of customer enthusiasm and demand than they are seeing now. One 2-day bootcamp with a construction company provided a use case with $10 million of savings. US Government business is slow, but business is expected to accelerate later this year due to timing of contracts. Still, its the US Commercial busines that has me excited as I don’t feel the good news is yet reflected in the stock price. In terms of revenue last qtr: Palantir (PLTR) delivered a blockbuster quarter with its commercial business here in America. Last quarter US Commercial revenue spiked 70% year-over-year as customer count jumped 55% from a year ago. And business is bound to get better as US Commercial Total Contact Velue (TCV) lept 107%. What caused this spike? Palantir’s AIP Bootcamps, a 5 day bootcamp for the company to understand (1) how to apply AI to its operations (2) develop use casses and (3) onboard and train users. The company has already done 560 bootcamps with 465 organizations just this year. Management has never seen this level of customer enthusiasm and demand than they are seeing now. One 2-day bootcamp with a construction company provided a use case with $10 million of savings. US Government business is slow, but business is expected to accelerate later this year due to timing of contracts. Still, its the US Commercial busines that has me excited as I don’t feel the good news is yet reflected in the stock price. In terms of revenue last qtr:

Palantir takes a customers data and/or public data and solves complex problems that a regular program can’t solve. Examples include predicting things on the battlefield, where to seat passengers on a flight, logistics for COVID-19 vaccines, or how much product (i.e. candy bars) can be sold to different areas around the world — depending on the weather — and if you’re missing one key ingredient for that candy bar, which customers will be affected most and by how much. Management says what’s most exciting about Palantir is the ability to launch products that are literally the only products on the market that will change your life and determine who fails across enterprise, both government and commercial (source: 2023 Q1 Earnings Call). Palantir has built three principal software platforms:

PLTR has an excellent Estimated Long Term Growth Rate of 85% but that’s an analyst estimate for profit growth, not stock growth (and certainly not revenue growth). But keep in mind profits are slight so it’s easy to compound. The P/E of 70 is high, but I value the stock on a price to sales basis. PLTR will be added to the Growth Portfolio as the uptick in US Commercial business is a catalyst. |

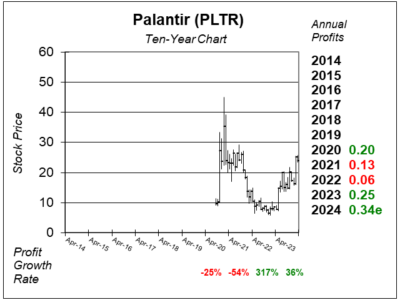

One Year Chart |

This stock spiked after earnings on HUGE VOLUME. That got my attention. At first I felt the stock was fairly valued (and it is) but this surge in commercial busines might cause estimates to increase in the coming quarters. This stock spiked after earnings on HUGE VOLUME. That got my attention. At first I felt the stock was fairly valued (and it is) but this surge in commercial busines might cause estimates to increase in the coming quarters.

PLTR has a P/E of 70, up from 67 last qtr. That’s a high P/E But I price this stock on a price-to-sales ratio. More on the valuation later. The Est. LTG is 85% this qtr. That’s an estimated 3-5 year profit growth estimate. Profits are growing great right now, but the EPS are still small. |

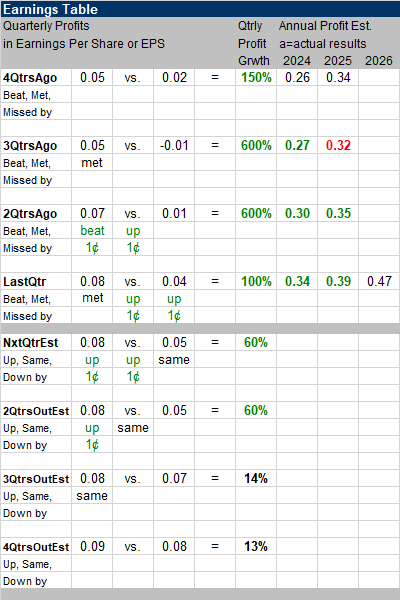

Earnings Table |

Last qtr, Palantir recorded 100% profit growth as it delivered a profit of $0.08 versus $0.04 a year ago. Revenue increased 20%, year-over-year versus estimates of 18%. Customer count increased 35% year-over-year, while US commercial customer count grew 55%. Last qtr, Palantir recorded 100% profit growth as it delivered a profit of $0.08 versus $0.04 a year ago. Revenue increased 20%, year-over-year versus estimates of 18%. Customer count increased 35% year-over-year, while US commercial customer count grew 55%.

Growth was driven by 32% growth in commercial revenue and 11% government revenue. Revenue from the top customers is still growing, with the trailing 12-month revenue per customer from the top 20 customers expanding 11% year-over-year. PLTR’s TCV booked was $1.15 billion, up 192% year-over-year. This means that there’s a huge pipeline of business coming in future quarters. Customer count grew 35% last year. Annual Profit Estimates are up this quarter. They should be up a lot more. Qtrly Profit Estimates are for 60%, 60%, 14%, and 13% profit growth the next 4 qtrs. Analysts think revenue will grow 19% next qtr. |

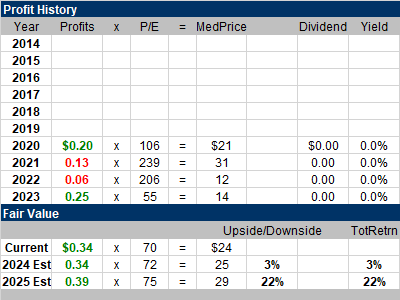

Fair Value |

PLTR had its IPO in September 2020, and at the end of September ended the month at $9.50 with a market cap of $16.4 billion. PLTR did $772 million in sales that year, thus the stock was selling for 21x 2020 revenue at the time. PLTR had its IPO in September 2020, and at the end of September ended the month at $9.50 with a market cap of $16.4 billion. PLTR did $772 million in sales that year, thus the stock was selling for 21x 2020 revenue at the time.

This qtr, PLTR sells for 19x 2023 revenue estimates. My Fair Value is 20x revenue estimates, or $25 a share for 2024: Current: 2024 Fair Value: 2025 Fair Value: |

Bottom Line |

Palantir (PLTR) was at one time one of the hottest IPOs of 2020. It’s software is unique and can deliver results other companies can not. But back then, the company wasn’t making profits. Now, management is committed to profitability. So the stock is doing better than it did in 2022. Palantir (PLTR) was at one time one of the hottest IPOs of 2020. It’s software is unique and can deliver results other companies can not. But back then, the company wasn’t making profits. Now, management is committed to profitability. So the stock is doing better than it did in 2022.

Palantir’s US commercial business showed great results last qtr due to the rollouts of bootcamps, which make the decision making easy. Although the shares are fairly valued here around $24, I feel I need to follow the big money into the stock. PLTR will be added to the Growth Portfolio and rank 18th in the Power Rankings. |

Power Rankings |

Growth Stock Portfolio

18 of 32Aggressive Growth Portfolio N/AConservative Stock Portfolio N/A |