Stock (Symbol) |

NVIDIA (NVDA) |

Stock Price |

$180 |

Sector |

| Technology |

Data is as of |

| March 3, 2026 |

Expected to Report |

| May 27 |

Company Description |

NVIDIA Corporation is a full-stack computing infrastructure company. NVIDIA Corporation is a full-stack computing infrastructure company.

The Company is engaged in accelerated computing to help solve the challenging computational problems. The Company’s segments include Compute & Networking and Graphics. The Compute & Networking segment includes its Data Center accelerated computing platforms and artificial intelligence (AI) solutions and software; networking; automotive platforms and autonomous and electric vehicle solutions; Jetson for robotics and other embedded platforms, and DGX Cloud computing services. The Graphics segment includes GeForce GPUs for gaming and PCs, the GeForce NOW game streaming service and related infrastructure, and solutions for gaming platforms; Quadro/NVIDIA RTX GPUs for enterprise workstation graphics; virtual GPU software for cloud-based visual and virtual computing; automotive platforms for infotainment systems, and Omniverse Enterprise software for building and operating industrial AI and digital twin applications. Source: Refinitiv |

Sharek’s Take |

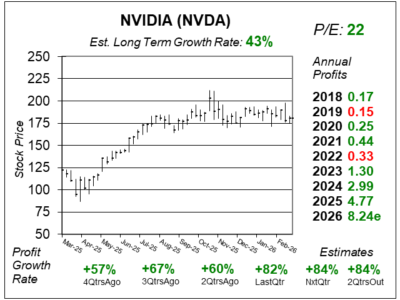

NVIDIA (NVDA) continues to see explosive demand for AI infrastructure as customers rapidly deploy its new Blackwell AI systems across global data centers. Last qtr, the company delivered 82% profit growth on 73% revenue growth, Data Center revenue — accounted for 90% of the total revenue — was up 75% year-over-year, driven by strong adoption of Blackwell and the ramp of Grace Blackwell NVL72 systems, a rack-sized AI supercomputer for very large AI systems. Management stated demand is now expanding beyond AI training as companies increasingly deploy GPUs for AI inference, where models generate responses and run real-world applications. This shift is driving massive infrastructure buildouts, with cloud providers expected to spend nearly $700 billion on data center CapEx in 2026. NVIDIA was originally focused on the computer graphics market, and invented the first graphics processing unit (GPU) in 1999 which made the company the leader in computer graphics. The company introduced its CUDA programming model in 2006 and ushered in parallel processing of its GPU for high-performance computing that could be used in fields including aerospace, biotechnology, and energy exploration. NVDA has since expanded its architecture to scientific computing, artificial intelligence, data science, autonomous vehicles, robotics, and virtual reality (or AR). NVDA has four operating segments : Gaming, Data Center, Professional Visualization and Auto. NVIDIA’s rapid growth was originally due to its superior gaming chips, and is now driven by its Data Center segment, due to the strong demand for Generative AI platforms. Here are segment stats from last qtr:

NVIDIA is in a golden era of a universal upgrade in computing. The CEO breaks down the four previous eras as (1) PC lead by IBM, (2) Internet, (3) Mobile & Cloud lead by the iPhone, and (4) AI. Analysts give NVDA an Estimated Long Term Growth Rate (Est. LTG) of 43% a year. For 2026, NVDA returned $41 billion to its shareholders in the form of share repurchases and dividends. NVIDIA is the top holding in my Growth Portfolio and Aggressive Growth Portfolio. The next big thing in AI will be the NVL 72 supercycle. The NVIDIA GB200 NVL 72 is a rack system with slots for components. Inside are 36 NVIDIA Grace CPUs and 72 NVIDIA Blackwell GPUs, which are connected by NVIDIA’s NVLink, a spine (the size of a 4×6 beam of wood) with two miles of cables (5000 total). |

One Year Chart |

NVIDIA stock has been basing around $175 – $200. The NASDAQ is currently under pressure, but with NVDA’s superior profit growth, I expect this stock to be one of the first leaders of the next market upswing. NVIDIA stock has been basing around $175 – $200. The NASDAQ is currently under pressure, but with NVDA’s superior profit growth, I expect this stock to be one of the first leaders of the next market upswing.

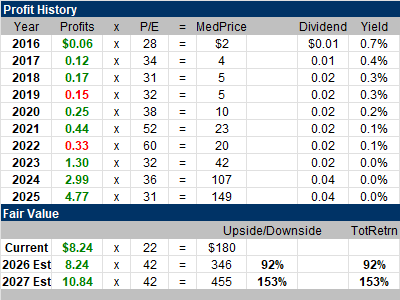

This stock has a P/E of 22. My Fair Value is a 42 PE. I think the stock is very undervalued. The P/E was 24 last quarter. The Est. LTG is 43%, up from 40% 2QtrsAgo. The Est. LTG is analysts’ 3-5 year guess of annual profit growth (not stock growth). Quarterly profit growth has been rapid the past 4 qtrs. And Estimates are for rapid growth to continue. |

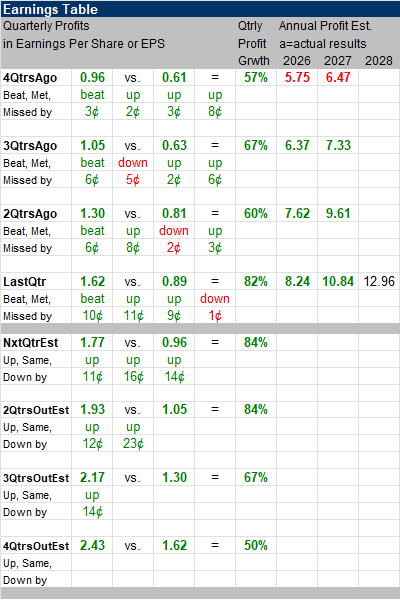

Earnings Table |

Last qtr, NVIDIA reported 82% profit growth and beat estimates of 71%. Revenue grew 73% and beat analyst’s estimates of 67%. Gross margin was 75.2%, up from 73.5% year ago. Last qtr, NVIDIA reported 82% profit growth and beat estimates of 71%. Revenue grew 73% and beat analyst’s estimates of 67%. Gross margin was 75.2%, up from 73.5% year ago.

Annual Profit Estimates increased by a good amount this qtr. Qtrly Profit Estimates for the next 4 qtrs are 84%, 84%, 67%, and 50%. That’s impressive. For next qtr, analysts predict revenue will climb 78% year-over-year. |

Fair Value |

NVDA has a P/E of 22. I think the stock is very cheap and has the ability to go on a run higher once the stock market goes into an uptrend. NVDA has a P/E of 22. I think the stock is very cheap and has the ability to go on a run higher once the stock market goes into an uptrend.

My Fair Value is a P/E of 42, and when we plug in 2026 profit estimates, we get a Fair Value of $346 a share, 92% higher than the recent quote of $180. There’s ample upside for 2027 — 153% — as my guess is the stock could be $455 by then. |

Bottom Line |

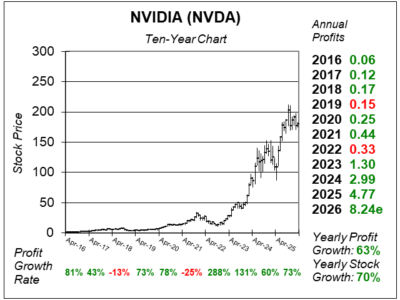

NVIDIA (NVDA) stock has had a rocky decade. In 2016, the NVDIA GeForce video processor created a surge in revenue and profits and helped the stock soar from $0.82 to $2.67 that year (after accounting for stock-splits). NVIDIA continued to rise into 2018 and peaked at $7. Then the stock fell to $3 in late-2018 as the company had lots of returns of its high-end processors as the price of Bitcoin declined and crypto miners returned their gear back to NVIDIA. Note profits fell in 2019. NVIDIA (NVDA) stock has had a rocky decade. In 2016, the NVDIA GeForce video processor created a surge in revenue and profits and helped the stock soar from $0.82 to $2.67 that year (after accounting for stock-splits). NVIDIA continued to rise into 2018 and peaked at $7. Then the stock fell to $3 in late-2018 as the company had lots of returns of its high-end processors as the price of Bitcoin declined and crypto miners returned their gear back to NVIDIA. Note profits fell in 2019.

Meanwhile, the 2022 slump was due to a downturn in sales in the Gaming division as (1) businesses were flush with cash in 2021 and had already upgraded computers and (2) Bitcoin miners found it unprofitable to mine with lower crypto prices combined with high electricity costs. In January 2023 the stock pushed past $20 and ended that year at $50 as Datacenter sales pushed higher due to AI investments. 2024 was also great as the shares went from $50 to 134. NVIDIA is still the top stock in my universe. Another sensational quarter. NVDA ranks first in the Growth Portfolio and Aggressive Growth Portfolio Power Rankings. |

Power Rankings |

Growth Stock Portfolio

1 of 29Aggressive Growth Portfolio 1 of 18Conservative Stock Portfolio N/A |