Stock (Symbol) |

McDonald’s (MCD) |

Stock Price |

$268 |

Sector |

| Retail & Travel |

Data is as of |

| May 9, 2024 |

Expected to Report |

| July 25 |

Company Description |

McDonald’s Corporation (McDonald’s) operates and franchises McDonald’s restaurants. McDonald’s Corporation (McDonald’s) operates and franchises McDonald’s restaurants.

The Company’s restaurants serve a locally relevant menu of food and beverages. The Company’s segments include United States (U.S.), International Operated Markets (IOM) and International Developmental Licensed Markets & Corporate (IDL). The U.S. segment focuses on Company’s menu and offerings, as well as delivery and digital platforms. Its IOM segment includes its operations in markets, such as Australia, Canada, France, Germany, Italy, the Netherlands, Spain, and the United Kingdom. Its IDL segment includes its operations in markets, such as Latin America and Asia. Its digital offerings include drive thru, takeaway, delivery, curbside pick-up, and dine-in. Its menu includes hamburgers and cheeseburgers, Big Mac, Quarter Pounder with Cheese, Filet-O-Fish, wraps, shakes, soft drinks, coffee, McCafe beverages and other beverages. Source: Refinitiv |

Sharek’s Take |

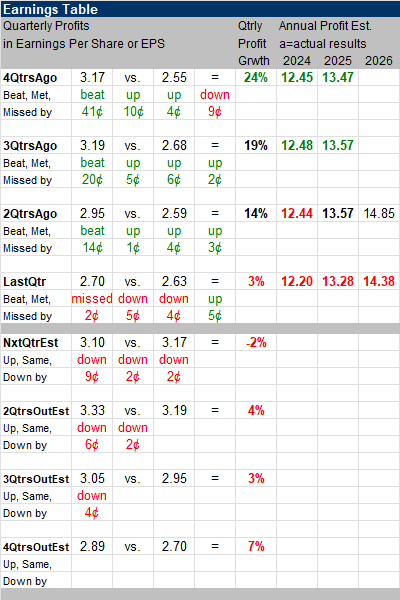

McDonald’s (MCD) is introducing a $5 value meal to help boost sales as customers are strapped for cash. As CNBC reported, the mean will consist of a 4 piece chicken nugget, fries, a Coke (which is co-sponsoring), and either a McChicken or McDouble. The promotion will begin on June 24 and last a month. Sales increased just 3% last quarter. Meanwhile, profit growth has slowed from 19% three qtrs ago to 14% two qtrs ago, and 3% last quarter. Next quarter’s profit growth estimate is -2%. The management said in the earnings call that there was flat or declining industry traffic in major markets like the US, Australia, Canada, Germany, Japan, and the UK with customers becoming “even more discriminating with every dollar that they spend.” Meanwhile, the company aims to accelerate restaurant openings and reach 50,000 locations by the end of 2027. They are off to a strong start, with recent milestones like opening their 6,000th restaurant in China. McDonald’s (MCD) is introducing a $5 value meal to help boost sales as customers are strapped for cash. As CNBC reported, the mean will consist of a 4 piece chicken nugget, fries, a Coke (which is co-sponsoring), and either a McChicken or McDouble. The promotion will begin on June 24 and last a month. Sales increased just 3% last quarter. Meanwhile, profit growth has slowed from 19% three qtrs ago to 14% two qtrs ago, and 3% last quarter. Next quarter’s profit growth estimate is -2%. The management said in the earnings call that there was flat or declining industry traffic in major markets like the US, Australia, Canada, Germany, Japan, and the UK with customers becoming “even more discriminating with every dollar that they spend.” Meanwhile, the company aims to accelerate restaurant openings and reach 50,000 locations by the end of 2027. They are off to a strong start, with recent milestones like opening their 6,000th restaurant in China.

Here are some highlights from the last qtr:

McDonald’s is the world’s leading global food service retailer with over 40,000 locations in over 100 countries. In a typical franchise arrangement, McDonald’s owns the real estate, long-term lease on the land, and building with the franchisee paying for equipment, signs, seating, and decor. Currently, franchised restaurants represent 95% of McDonald’s restaurants worldwide. The company recently modernized its U.S locations via its Experience the Future (EOTF) remodeling campaign which incorporates a modern look and McCafe dessert counters, and digital self-service kiosks. Mobile order and pay are also bringing phone technology into the fold with faster counter service. Digital sales continue to improve productivity. This company is thriving off of innovation. McDonald’s ranked second in Fast Company’s World’s Most Innovative Companies for 2023. MCD is one of the safest stocks in the world but it’s a typically a slow grower. The Estimated Long Term Growth Rate is 7% and stock also yields just over 2%. But profits had been rising faster than 10% recently. In October 2023 management approved a 10% cash dividend increases, the 47th consecutive year of dividend increases. And in Fiscal 2022, management returned $3.9 billion in stock buybacks and paid $4.2 billion in cash dividends to shareholders. McDonald’s is part of the Conservative Growth Portfolio. The company has lost its momentum. |

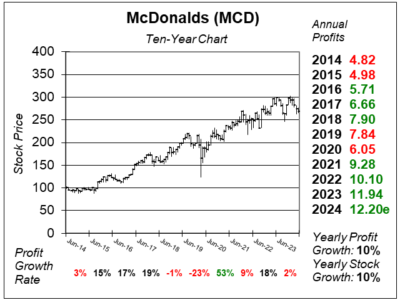

One Year Chart |

This company had been growing profits briskly, But that trend ended last quarter. Looking ahead, the company has tough comparisons. So I expect profits to be weak the next few quarters. This company had been growing profits briskly, But that trend ended last quarter. Looking ahead, the company has tough comparisons. So I expect profits to be weak the next few quarters.

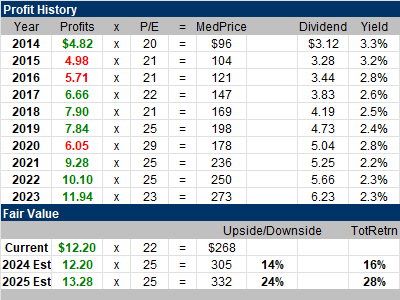

The 22 P/E is good. My Fair Value is a P/E of 25, or $305 a share. The Est. LTG is just 7%. Same as last quarter. I consider MCD to be a 10-12% grower. Qtrly profit growth has been good. 3% last quarter. Estimates are for single digits in the coming qtrs but the company has been beating the street. |

Earnings Table |

Last qtr, McDonald’s reported 3% profit growth, just as expected. Revenue increased 5%, year-on-year, and met estimates of 5%. Sales increased 3%. Same-store sales increased by 2% with 3% growth in US and International Operating markets and flat growth in International Developmental markets. Last qtr, McDonald’s reported 3% profit growth, just as expected. Revenue increased 5%, year-on-year, and met estimates of 5%. Sales increased 3%. Same-store sales increased by 2% with 3% growth in US and International Operating markets and flat growth in International Developmental markets.

US sales growth was driven by higher average checks from menu price hikes. Growth in international company-operated markets was led by U.K. and Germany, but this was partly offset by negative sales in France. International Developmental Licensed Markets segment had no growth due to ongoing war in the Middle East conflict outweighed positive sales in Japan, Latin America, and Europe. Annual Profit Estimates decreased this quarter. Qtrly Profit Estimates for the next 4 qtrs are -2%, 4%, 3%,and 7%. Analysts think that MCD revenue will grow 2% next qtr. |

Fair Value |

My Fair Value P/E comes down a bit from 26 to 25. My Fair Value P/E comes down a bit from 26 to 25.

MCD has 14% upside to my 2024 Fair Value of $305. |

Bottom Line |

McDonald’s (MCD) is a true Blue Chip with a high degree of safety and a dividend that’s increased for 47 straight years. The ten-year chart is beautiful. McDonald’s (MCD) is a true Blue Chip with a high degree of safety and a dividend that’s increased for 47 straight years. The ten-year chart is beautiful.

MCD is a “value” again. The $ meal deal will drive demand (for a month), but the company has been raising prices and taking away value meals for a couple of years now. I think consumers just want a better deal, even if its more than $5. MCD stays at 10th in the Conservative Portfolio Power Rankings. I’m surprised its this high, but the upside is better than a lot of my other safe stocks. |

Power Rankings |

Growth Stock Portfolio

N/AAggressive Growth Portfolio N/AConservative Stock Portfolio 10 of 24 |