Stock (Symbol) |

McDonald’s (MCD) |

Stock Price |

$206 |

Sector |

| Retail & Travel |

Data is as of |

| March 3, 2021 |

Expected to Report |

| April 28 |

Company Description |

McDonald’s franchises and operates McDonald’s restaurants in 119 countries globally. All restaurants are operated either by the Company or by franchisees. Under the conventional franchise arrangement, franchisees provide a portion of the capital required by initially investing in the equipment, signs, seating and decor of their restaurant businesses, and by reinvesting in the business over time. MCD owns the land and building or secures long-term leases for both Company-operated and conventional franchised restaurant sites. Source: Thomson Financial McDonald’s franchises and operates McDonald’s restaurants in 119 countries globally. All restaurants are operated either by the Company or by franchisees. Under the conventional franchise arrangement, franchisees provide a portion of the capital required by initially investing in the equipment, signs, seating and decor of their restaurant businesses, and by reinvesting in the business over time. MCD owns the land and building or secures long-term leases for both Company-operated and conventional franchised restaurant sites. Source: Thomson Financial |

Sharek’s Take |

McDonald’s (MCD) should have a great year ahead as the worldwide economy reopens as COVID-19 vaccines become more prominent. Here in New York City, the McDonald’s locations have been mostly empty for the past year. You can go into the restaurants and order to go with either a kiosk or the cashier. But there is no sit-down dining. And there really aren’t many people getting take-out anyway. Last qtr, MCD had -14% profit growth as revenue growth was -2% with -1% same store sales growth. The company has recovered 99% of its 2019 same store sales, and is continuing to see improvement. Analysts have pushed 2021 profit estimates up from $7.88 to $8.43 the past four qtrs, and I feel these estimates are likely to keep rising. McDonald’s (MCD) should have a great year ahead as the worldwide economy reopens as COVID-19 vaccines become more prominent. Here in New York City, the McDonald’s locations have been mostly empty for the past year. You can go into the restaurants and order to go with either a kiosk or the cashier. But there is no sit-down dining. And there really aren’t many people getting take-out anyway. Last qtr, MCD had -14% profit growth as revenue growth was -2% with -1% same store sales growth. The company has recovered 99% of its 2019 same store sales, and is continuing to see improvement. Analysts have pushed 2021 profit estimates up from $7.88 to $8.43 the past four qtrs, and I feel these estimates are likely to keep rising.

McDonald’s s is the world’s leading global foodservice retailer with over 39,000 locations in over 100 countries. Company management is doing a fantastic job bringing the restaurants into the digital age. Locations being modernized with new technology like kiosks and apps. Food delivery is also enhancing same store sales. And although the core menu is 70% of food sales across top markets, developing a reputation for great chicken represents one of management’s highest ambitions. Last month the company launched its new Chicken sandwiches (which I heard are good but still not on Popoye’s level). Here’s a few bullet points on what’s new:

MCD is one of the safest stocks in the world — this is a stock you can buy-and-hold for decades without having to worry about it — but it’s a slow grower. The stock rose 10% a year the past decade and the Estimated Long Term Growth Rate is 13% a year. I think of MCD as a “10% grower”. The stock also yields 2.5%. The dividend was just increased 3% in October 2020 to $5.16 per year, the 44th consecutive year of increases. From 2006-2019 MCD returned $25 billion to shareholders by paying out $10 billion in dividends and buying back $15 billion in stock (a 10% reduction of shares outstanding). In early March 2020, the Company voluntarily suspended share repurchases from the open market. McDonald’s is part of the Conservative Growth Portfolio. A robust economy awaits us in the 2nd half of 2021, and more travel & entertainment will mean more eating out. |

One Year Chart |

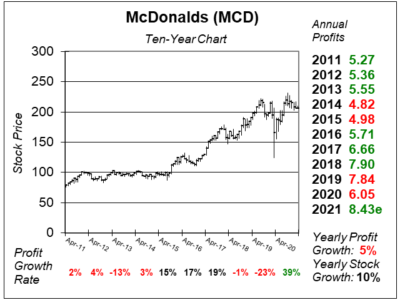

MCD got hot last October. MCD got hot last October.

The Est. LTG increased from 3% to 4% to 5% the past three qtrs. But if you look at the stock’s history, this figure used to be 7% to 9%. I think MCD is a 10% grower. The P/E of 26 is higher than normal for this stock, but I think that’s a fair valuation because I feel profits will come in better than expected in 2021. |

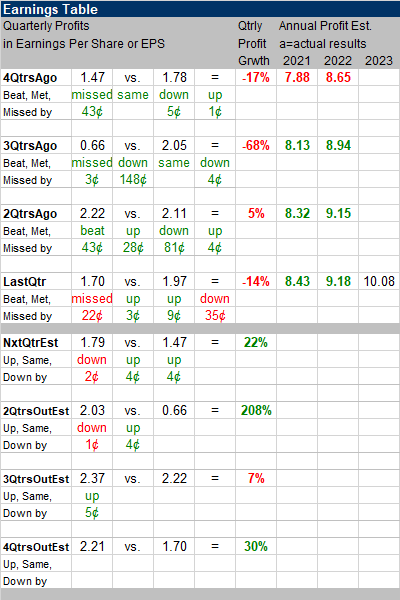

Earnings Table |

Last qtr, MCD had -14% profit growth as revenue growth was -2% with -1% same store sales growth. U.S. same store sales growth was a solid 6% last qtr, but International Operated Markets had -7% growth as most countries have had COVID-19 government restrictions that have carried over into 2021. The McRib, Buy One, Get One for $1 and a new bakery line fueled momentum. Last qtr, MCD had -14% profit growth as revenue growth was -2% with -1% same store sales growth. U.S. same store sales growth was a solid 6% last qtr, but International Operated Markets had -7% growth as most countries have had COVID-19 government restrictions that have carried over into 2021. The McRib, Buy One, Get One for $1 and a new bakery line fueled momentum.

Annual Profit Estimates increased for the 3rd straight qtr. I feel MCD will start having some great qtrs as vaccines should be readily available by next month. Qtrly profit Estimates for the next 4 qtrs are 22%, 208%, 7%, and 30%. Management stated January U.S. same store sales will likely be in the high single-digits. That could mean the company beats the street this qtr. |

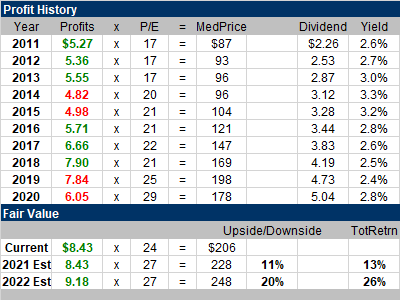

Fair Value |

My Fair Value is a P/E of 27, which is above where I would normally put it (23-25). Last qtr my Fair Value P/E was 28, as these 2021/2022 estimates were way too low. Now that these figures have increased, I’m simmering down my Fair Value P/E. My Fair Value is a P/E of 27, which is above where I would normally put it (23-25). Last qtr my Fair Value P/E was 28, as these 2021/2022 estimates were way too low. Now that these figures have increased, I’m simmering down my Fair Value P/E.

My current 2021 Fair Value is $228, which is 11% upside for this year and 20% upside by next year. MCD also pays a nice dividend yield that’s close to 2.5%. |

Bottom Line |

McDonald’s (MCD) is a true Blue Chip with a high degree of safety and a dividend that’s increased for more than 40 straight years. McDonald’s (MCD) is a true Blue Chip with a high degree of safety and a dividend that’s increased for more than 40 straight years.

With more COVID-19 vaccines being distributed now, I expect America will be open for robust travel in April or May. That should mean more traffic in McDonald’s locations. I expect same store sales numbers could look great compared to a year-ago. MCD moves up from 29th to 24th the Conservative Portfolio Power Rankings. |

Power Rankings |

Growth Stock Portfolio

N/AAggressive Growth Portfolio N/AConservative Stock Portfolio 24 of 35 |