Stock (Symbol) |

Broadcom (AVGO) |

Stock Price |

$250 |

Sector |

| Technology |

Data is as of |

| December 16, 2024 |

Expected to Report |

| March 5 |

Company Description |

It operates through two segments: semiconductor solutions and infrastructure software. Its semiconductor solutions segment includes semiconductor solution product lines, as well as its Internet protocol (IP) licensing. It provides semiconductor solutions for managing the movement of data in data center, telecom, enterprise and embedded networking applications. It also provides a variety of radio frequency (RF) semiconductor devices, wireless connectivity solutions and custom touch controllers for the wireless market. Its infrastructure software segment includes its mainframe, distributed and cyber security solutions, and its fiber channel storage area networking (FC SAN) business. Its mainframe software provides DevOps, AIOps, Security and Data Management Systems solutions. Source: Refinitiv |

Sharek’s Take |

Broadcom (AVGO) stock surged from ~$100 to ~$250 during the past year as the company got recognized for its AI superiority. AVGO is making AI chips with less heat that consumer less power than some competitors. Its method for building AI infrastructure is different than NVIDIA’s, as its building a general datacenter product that fits everyone’s needs, using hardware from different manufacturers. Broadcom specializes in energy-efficient AI networks using ASICs instead of power-hungry GPUs. In addition, Broadcom refers to AI accelerators as XPU’s instead of GPUs, focusing on compute memory, I/O precision, and software-optimized packaging for efficient performance. In 2024, AVGO’s AI accelerator revenue (XPUs and Networking) grew 220% from $4 billion to $12 billion. Broadcom is a semiconductor and software company that designs thousands of products for home connectivity, cloud data centers, and enterprise businesses. It is a conglomerate that was formed over 50 years of mergers and acquisitions including old-school tech companies AT&T/Bell Labs, Lucent, Hewlett-Packard and its semiconductor division, and younger industry leaders (including Broadcom, LSI, Broadcom Corporation, Brocade, CA Technologies and Symantec). The majority of AVGO’s silicon wafer manufacturing operations are designed in North America or Europe, then outsourced by the company to external foundries in Asia, such as Taiwan Semiconductor. Broadcom’s method for building AI infrastructure is different, as its building a general product that fits everyone’s needs, with hardware from different manufacturers used in the datacenter:

AVGO has two business segments:

AVGO stock has an Estimated Long-Term-Growth (LTG) Rate of 20%, but the P/E of 40 makes the stock overvalued by 13%, in my opinion. AVGO also pays a nice dividend of 2%, and management buys back stock. The company has a dividend policy of pacing 50% of the prior-year’s free cash flow to investors. Since 2016, AVGO’s dividend has grown around 20% a year. AVGO is part of the Growth Portfolio and Aggressive Growth Portfolio. |

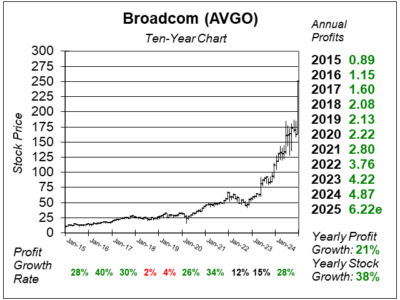

One Year Chart |

AVGO stock soared after last qtr’s earnings were released, but management has been explaining how great its AI achievements have been for many months. AVGO stock soared after last qtr’s earnings were released, but management has been explaining how great its AI achievements have been for many months.

This stock has a 40 P/E this quarter. The P/E was just 26 last quarter as its gone from undervalued to overvalued (in my opinion). The Est. LTG is 20%, same as last qtr. Qtrly profit growth was poor around a year ago as AVGO swallowed up the big VMware acquisition. Note profits are expected to climb around 35% the next 2 qtrs. Maybe 40%? |

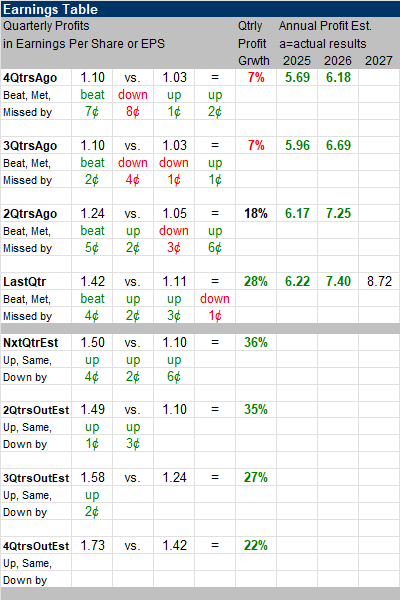

Earnings Table |

Last qtr, Broadcom posted 28% profit growth and beat expectations of 24% growth. Revenue increased 51% from a year ago, a beat from the analysts expectation of 44%. But this was helped by the acquisition of Vmware. Excluding VMware, revenue rose 11%. Last qtr, Broadcom posted 28% profit growth and beat expectations of 24% growth. Revenue increased 51% from a year ago, a beat from the analysts expectation of 44%. But this was helped by the acquisition of Vmware. Excluding VMware, revenue rose 11%.

Annual Profit Estimates increased this qtr. Qtrly Profit Estimates for the next 4 qtrs are 36%, 35%, 27%, and 22%. These are excellent numbers! For next qtr, analysts expect revenue to grow 22%. |

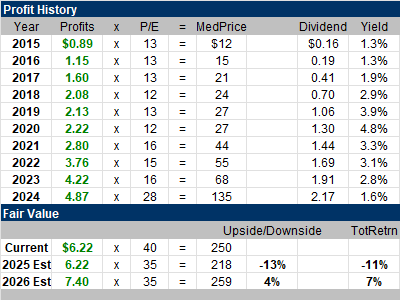

Fair Value |

AVGO stock has been undervalued for a decade now. I bought it for clients in March 2022 around $600 when the P/E was 17.3. AVGO stock has been undervalued for a decade now. I bought it for clients in March 2022 around $600 when the P/E was 17.3.

My Fair Value on AVGO is a P/E of 35. The stock has a P/E of 40. At $250 this quarter, the stock is 13% above my 2025 Fair Value of 218 a share. |

Bottom Line |

Broadcom (AVGO) has a great looking ten-year chart. Recent success made the shares go parabolic, so its dangerous to take a big position now. Broadcom (AVGO) has a great looking ten-year chart. Recent success made the shares go parabolic, so its dangerous to take a big position now.

Broadcom is a core holding for AI investors. It’s AI semiconductors are in high demand. I could be wrong, but ts as if AVGO is picking up the low-end AI market share while NVDA is the high-end supplier. On the downside, the stock has gone on a parabolic run making it dangerous to buy here, and the shares seem slightly overvalued. AVGO drops from 7th to 9th in the Growth Portfolio Power Rankings. The stock drops from 4th to 12th in the Aggressive Growth Portfolio Power Rankings. I purchased AVGO for this portfolio last quarter, and the stock has since jumped in price, thus its not the buy it used to be. |

Power Rankings |

Growth Stock Portfolio

9 of 30Aggressive Growth Portfolio 12 of 15Conservative Stock Portfolio N/A |