Stock (Symbol) |

MercadoLibre (MELI) |

Stock Price |

$1730 |

Sector |

| Retail & Travel |

Data is as of |

| December 23, 2024 |

Expected to Report |

| February 20 |

Company Description |

Mercado Libre Inc is a Uruguay-based e-commerce business facilitator of Argentinian origins. Mercado Libre Inc is a Uruguay-based e-commerce business facilitator of Argentinian origins.

The e-commerce products enable retail and wholesale via Internet platforms designed to provide users with a portfolio of services to facilitate commercial transactions. The Company’s geographic coverage includes 18 countries of Latin America. The primary offer is an ecosystem of six integrated e-commerce services: the Mercado Libre Marketplace, the Mercado Libre Classifieds service, the Mercado Pago payments solution, the Mercado Credito financial solutions, the Mercado Envios logistic solutions including shipping, the Mercado Ads advertising platform and the Mercado Shops digital storefront solution. Source: Refinitiv |

Sharek’s Take |

MercadoLibre (MELI) continues to have strong momentum in South America. Revenue grew 35% last quarter, including 51% in ecommerce and 25% growth in Fintech. But the company delivered just 9% profit growth last qtr, prioritizing long term investments in logistics and technology. The company opened 6 new fulfillment senators last qtr (5 in Brazil and 1 in Mexico). MELI continue grow its Mercado Credito credit card, as its credit portfolio rose 77% compared to a year ago. MercadoLibre (MELI) continues to have strong momentum in South America. Revenue grew 35% last quarter, including 51% in ecommerce and 25% growth in Fintech. But the company delivered just 9% profit growth last qtr, prioritizing long term investments in logistics and technology. The company opened 6 new fulfillment senators last qtr (5 in Brazil and 1 in Mexico). MELI continue grow its Mercado Credito credit card, as its credit portfolio rose 77% compared to a year ago.

MercadoLibre is the largest online commerce platform in Latin America and gives users a portfolio of services to do commercial transactions. The company is like South America’s combination of eBay, PayPal, and Shopify rolled into one. Here’s a quick rundown of the company’s history:

Here are some business highlights from last qtr:

MELI’s numbers are exceptional, especially profit estimates for the years ahead. Analysts give the company an Estimated Long-Term Growth Rate of 38%. This company looks a lot like Amazon did when its profits began rolling in. Analysts estimate MELI’s profits to grow from $20 a share in 2023 to maybe $100 in 2028. A 45 P/E on $100 in profits would get this stock from around $1750 to $4500. MELI is a top holding in the Aggressive Growth Portfolio and Growth Portfolio. |

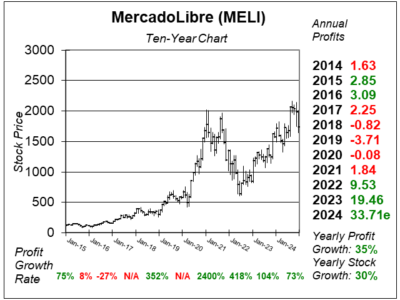

One Year Chart |

MELI stock fell after the company reported earnings and delivered just 9% profit growth, which missed estimates of 34%. Brazil’s economy has also been weak recently, which may have played a part in the stock’s decline. MELI stock fell after the company reported earnings and delivered just 9% profit growth, which missed estimates of 34%. Brazil’s economy has also been weak recently, which may have played a part in the stock’s decline.

The Est. LTG is 38%, and the P/E is just 38. I think the stock is a bargain here. I think company growing profits at 38% long-term might hyopothetically have a P/E around 60. Quarterly profit growth is often erratic. We have to accept this. |

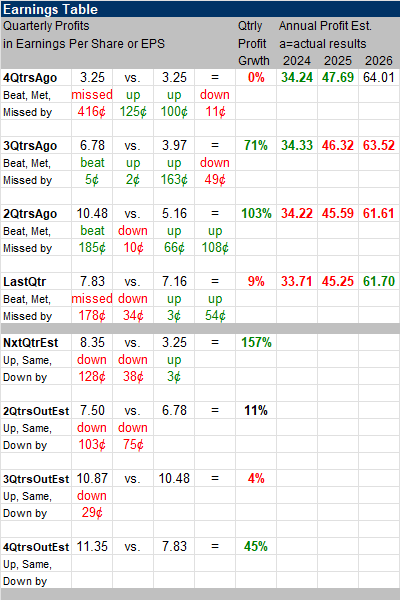

Earnings Table |

Last qtr, MercadoLibre reported 9% profit growth, missing the analyst’s expectation of 34% growth. Revenue increased 35%, year-over-year in US dollars against analyst estimates of 33%. Gross Profit Margin (excluding Argentina) was 43.3% vs. 50.9% a year ago due to investments in logistics. Operating Margin was 10.5%, down from 20.0% a year-ago. Last qtr, MercadoLibre reported 9% profit growth, missing the analyst’s expectation of 34% growth. Revenue increased 35%, year-over-year in US dollars against analyst estimates of 33%. Gross Profit Margin (excluding Argentina) was 43.3% vs. 50.9% a year ago due to investments in logistics. Operating Margin was 10.5%, down from 20.0% a year-ago.

Here’s geographic revenue growth from last qtr:

Annual Profit Estimates are down slightly this quarter: 2024: $33.71 Qtrly Profit Estimates are for 157%, 11%, 4%, and 45% profit growth the next 4 qtrs. Analysts think MELI revenue will grow 33% next quarter. Profit estimates are down as the company invests in its credit business, which increases upfront provisions. MELI is also investing in shipping. |

Fair Value |

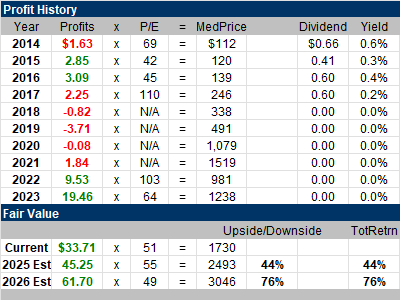

I’m pricing MELI on a price-to-sales basis as profits are low right now. Looking back to past years, MELI’s year-end price-to-sales ratio was: I’m pricing MELI on a price-to-sales basis as profits are low right now. Looking back to past years, MELI’s year-end price-to-sales ratio was:

2014: 10 This qtr, the stock sells for 4x 2024 revenue estimates, my Fair Value is 5x 2025 revenue: Current:4 x $20.4 billion revenue est = $88 billion market cap 2024 Fair Value: 2025 Fair Value: |

Bottom Line |

MercadoLibre (MELI) has been a wild stock the past five years. Overall this has been an excellent investment as MELI went public in 2007 and opened at $22 a share. MercadoLibre (MELI) has been a wild stock the past five years. Overall this has been an excellent investment as MELI went public in 2007 and opened at $22 a share.

MercadoLibre suffered a hiccup last quarter as management decided to invest to grow. Amazon did this 2-3 decades ago and it worked out spendidly for them. MELI ranks 2nd in the Growth Portfolio and Aggressive Growth Portfolio Power Rankings. |

Power Rankings |

Growth Stock Portfolio

2 of 30Aggressive Growth Portfolio 2 of 15Conservative Stock Portfolio N/A |