Stock (Symbol) |

Visa (V) |

Stock Price |

$79 |

Sector |

| Financial |

Data is as of |

| December 10, 2016 |

Expected to Report |

| Jan 26 – 30 |

Company Description |

Visa Inc. is a payments technology company. The Company is engaged in operating a processing network, VisaNet, which facilitates authorization, clearing and settlement of payment transactions across the world. The Company provides its services to consumers, businesses, financial institutions and governments in more than 200 countries and territories for electronic payments. The Company offers fraud protection for account holders and rapid payment for merchants. The Company provides a variety of payment solutions that support payment products that issuers can offer to their account holders, such as pay now with debit, pay ahead with prepaid or pay later with credit products. The Company offers a suite of digital, eCommerce and mobile products and services. Source: Thomson Financial Visa Inc. is a payments technology company. The Company is engaged in operating a processing network, VisaNet, which facilitates authorization, clearing and settlement of payment transactions across the world. The Company provides its services to consumers, businesses, financial institutions and governments in more than 200 countries and territories for electronic payments. The Company offers fraud protection for account holders and rapid payment for merchants. The Company provides a variety of payment solutions that support payment products that issuers can offer to their account holders, such as pay now with debit, pay ahead with prepaid or pay later with credit products. The Company offers a suite of digital, eCommerce and mobile products and services. Source: Thomson Financial |

Sharek’s Take |

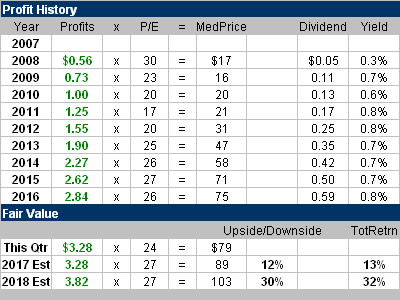

For the first time in a long time shares of Visa (V) are a good value. Shares of V used to be a good deal — back in the day. In the early part of the decade the company grew profits around 25% a year and the stock had a P/E of 17 to 20. Then in 2013 investors became more enamored with the shares and pushed the P/E up to the high 20s even as profit growth slowed into the high teens. The stock was then overvalued, and this led to flatlining the past couple of years. But now for the first time in a long time V is a deal again, as the P/E of 24 is the lowest I have seen it in a long time. Also, profits are expected to be solid the next 4 qtrs as the recently acquired Visa Europe and the new Costco Visa cards could be positive catalysts in the coming year. Overall, Visa is a solid investment for investors looking for growth and also those in need of safety. Profits have grown every year since the stock went public in 2008 and management buys back stock in addition to paying a dividend. Visa has a nice Estimated Long Term Growth Rate of 16% a year in addition to a 1% yield. I feel this stock is being overlooked with investors flooding into banks, but patient investors should note my 2018 Fair Value is 30% higher than the recent stock price. For the first time in a long time shares of Visa (V) are a good value. Shares of V used to be a good deal — back in the day. In the early part of the decade the company grew profits around 25% a year and the stock had a P/E of 17 to 20. Then in 2013 investors became more enamored with the shares and pushed the P/E up to the high 20s even as profit growth slowed into the high teens. The stock was then overvalued, and this led to flatlining the past couple of years. But now for the first time in a long time V is a deal again, as the P/E of 24 is the lowest I have seen it in a long time. Also, profits are expected to be solid the next 4 qtrs as the recently acquired Visa Europe and the new Costco Visa cards could be positive catalysts in the coming year. Overall, Visa is a solid investment for investors looking for growth and also those in need of safety. Profits have grown every year since the stock went public in 2008 and management buys back stock in addition to paying a dividend. Visa has a nice Estimated Long Term Growth Rate of 16% a year in addition to a 1% yield. I feel this stock is being overlooked with investors flooding into banks, but patient investors should note my 2018 Fair Value is 30% higher than the recent stock price. |

One Year Chart |

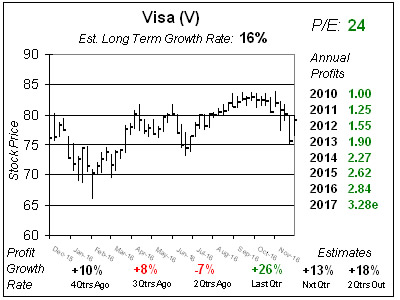

Visa had negative profit growth earlier in the year due to the acquisition of Visa Europe, but now the slower growth looks to be behind us. V clocked in with 26% profit growth last qtr, which shot past the 18% estimate, as sales increased a sparkling 19% helped by Visa Europe. Although Annual Profit Estimates declined a bit, analyst estimate profits will grow 13%, 18%, 20% and 13% the next 4 qtrs. In the chart, the stock didn’t do much in the past year as the P/E was high and growth was slow. Visa had negative profit growth earlier in the year due to the acquisition of Visa Europe, but now the slower growth looks to be behind us. V clocked in with 26% profit growth last qtr, which shot past the 18% estimate, as sales increased a sparkling 19% helped by Visa Europe. Although Annual Profit Estimates declined a bit, analyst estimate profits will grow 13%, 18%, 20% and 13% the next 4 qtrs. In the chart, the stock didn’t do much in the past year as the P/E was high and growth was slow. |

Fair Value |

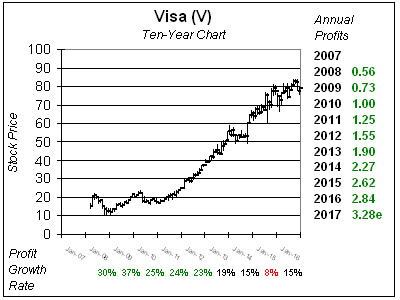

I’ve already discussed the undervalued/overvalued timeline of this stock above, but it’s nice to view the facts first hand. Notice the variance in Visa’s P/E from 2010-2012 vs 2013-2016. In the ten-year chart (below) you can see profit growth had slowed as the P/E increased. That was investors paying up for quality growth stocks. What gets me is this still is a quality growth stock. So I feel V should sell for 27x earnings and be $89. I’ve already discussed the undervalued/overvalued timeline of this stock above, but it’s nice to view the facts first hand. Notice the variance in Visa’s P/E from 2010-2012 vs 2013-2016. In the ten-year chart (below) you can see profit growth had slowed as the P/E increased. That was investors paying up for quality growth stocks. What gets me is this still is a quality growth stock. So I feel V should sell for 27x earnings and be $89. |

Bottom Line |

When you look at the big picture, Visa has been a solid investment for almost a decade now. Although the last two years haven’t amounted to much stock growth, the trend of the stock is still up. Now with the shares selling at a discount, I feel this is a ripe time for investors to purchase shares or increase their positions. V ranks 17th in the Growth Portfolio and Aggressive Growth Portfolio Power Rankings and 6th in the Conservative Portfolio Power Rankings. When you look at the big picture, Visa has been a solid investment for almost a decade now. Although the last two years haven’t amounted to much stock growth, the trend of the stock is still up. Now with the shares selling at a discount, I feel this is a ripe time for investors to purchase shares or increase their positions. V ranks 17th in the Growth Portfolio and Aggressive Growth Portfolio Power Rankings and 6th in the Conservative Portfolio Power Rankings. |

Power Rankings |

Growth Stock Portfolio

17 of 35Aggressive Growth Portfolio 17 of 18Conservative Stock Portfolio 6 of 29 |