Stock (Symbol) |

PayPal Holdings (PYPL) |

Stock Price |

$85 |

Sector |

| Financial |

Data is as of |

| August 17, 2018 |

Expected to Report |

| Oct 17 |

Company Description |

PayPal Holdings, Inc. is a technology platform and digital payments company that enables digital and mobile payments on behalf of consumers and merchants. The Company’s combined payment solutions, including its PayPal, PayPal Credit, Braintree, Venmo, Xoom and Paydiant products, compose its Payments Platform. It offers consumers person-to-person payment solutions through its PayPal Website and mobile application, Venmo and Xoom. Source: Thomson Financial PayPal Holdings, Inc. is a technology platform and digital payments company that enables digital and mobile payments on behalf of consumers and merchants. The Company’s combined payment solutions, including its PayPal, PayPal Credit, Braintree, Venmo, Xoom and Paydiant products, compose its Payments Platform. It offers consumers person-to-person payment solutions through its PayPal Website and mobile application, Venmo and Xoom. Source: Thomson Financial |

Sharek’s Take |

PayPal (PYPL) is delivering impressive results, but profit growth just slowed from 30% to 26% last qtr, and I feel it will be 22%-24% this qtr. Here’s a few bullet points from last qtr: PayPal (PYPL) is delivering impressive results, but profit growth just slowed from 30% to 26% last qtr, and I feel it will be 22%-24% this qtr. Here’s a few bullet points from last qtr:

Paypal has three catalysts:

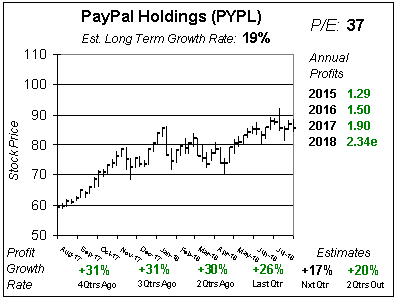

Last qtr PYPL was growing around 30% with a P/E of 35. This qtr it’s growing around 25% with a P/E of 37. Slower growth and a higher valuation — not good. I’m taking my Fair Value P/E down a bit from 37 to 35, which equates to $82 this year and $99 next year. The stock’s around $85 now, thus I don’t foresee much movement in the coming months. Still, this is a solid selection long-term. Growth is good and management also buys back billions in stock, but doesn’t pay dividends. |

One Year Chart |

PYPL tried to break out recently, but with slowing results it came back down. The Last qtr the company beat the street by 2 cents. It had previously beaten by 3 cents in each of the last 5 qtrs. Qtrly profit Estimates are 17%, 20%, 18% and 16%. If PYPL beats by 2-to-3 cents the next 4 qtrs that would mean low-20s growth. The Est. LTG of 19% is good but not great. The P/E was just 31 three qtrs ago, the stock was a better value then. PYPL tried to break out recently, but with slowing results it came back down. The Last qtr the company beat the street by 2 cents. It had previously beaten by 3 cents in each of the last 5 qtrs. Qtrly profit Estimates are 17%, 20%, 18% and 16%. If PYPL beats by 2-to-3 cents the next 4 qtrs that would mean low-20s growth. The Est. LTG of 19% is good but not great. The P/E was just 31 three qtrs ago, the stock was a better value then. |

Fair Value |

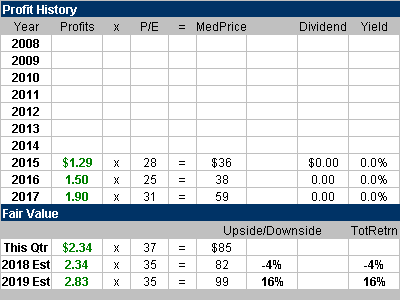

2018 estimates stayed the same this qtr. I don’t think a stock can get great momentum if annual estimates aren’t rising. My Fair Value P/E is getting cut a little this qtr, from 37 to 35. Last qrt my Fair Value was a stock price of $87 and I pretty much hit that on the head. This qtr it’s $82. 2018 estimates stayed the same this qtr. I don’t think a stock can get great momentum if annual estimates aren’t rising. My Fair Value P/E is getting cut a little this qtr, from 37 to 35. Last qrt my Fair Value was a stock price of $87 and I pretty much hit that on the head. This qtr it’s $82. |

Bottom Line |

PayPal continues to drive results higher as people are using their phone more and more to make purchases and send money. The stock’s been a good one since its IPO, but has had periods where it didn’t move much. I feel this is one of those times, and am not bullish on the shares at this time. This is still a solid buy-and-hold name with great growth opportunity, so I wouldn’t suggest selling out unless you have an itchy trigger finger that’s looking for immediate gratification. PYPL is ranked 30th in the Growth Portfolio Power Rankings. PayPal continues to drive results higher as people are using their phone more and more to make purchases and send money. The stock’s been a good one since its IPO, but has had periods where it didn’t move much. I feel this is one of those times, and am not bullish on the shares at this time. This is still a solid buy-and-hold name with great growth opportunity, so I wouldn’t suggest selling out unless you have an itchy trigger finger that’s looking for immediate gratification. PYPL is ranked 30th in the Growth Portfolio Power Rankings. |

Power Rankings |

Growth Stock Portfolio

30 of 39Aggressive Growth Portfolio N/AConservative Stock Portfolio N/A |