Stock (Symbol) |

Microsoft (MSFT) |

Stock Price |

$184 |

Sector |

| Technology |

Data is as of |

| May 25, 2020 |

Expected to Report |

| July 16 |

Company Description |

Microsoft Corporation is engaged in developing, licensing and supporting a range of software products and services. The Company also designs and sells hardware, and delivers online advertising to the customers. The Company operates in five segments: Devices and Consumer (D&C) Licensing, D&C Hardware, D&C Other, Commercial Licensing, and Commercial Other. Source: Thomson Financial Microsoft Corporation is engaged in developing, licensing and supporting a range of software products and services. The Company also designs and sells hardware, and delivers online advertising to the customers. The Company operates in five segments: Devices and Consumer (D&C) Licensing, D&C Hardware, D&C Other, Commercial Licensing, and Commercial Other. Source: Thomson Financial |

Sharek’s Take |

Microsoft (MSFT) just saw two years worth of digital transformations during the past two months. That means businesses that were taking their time getting up to speed with technology upgrades just whipped through the process during the COVID-19 stay-at-home period. What benefited the most from the process is Microsoft’s server products and cloud services as well as Office 365 (which just got changed to Microsoft 365). Microsoft (MSFT) just saw two years worth of digital transformations during the past two months. That means businesses that were taking their time getting up to speed with technology upgrades just whipped through the process during the COVID-19 stay-at-home period. What benefited the most from the process is Microsoft’s server products and cloud services as well as Office 365 (which just got changed to Microsoft 365).

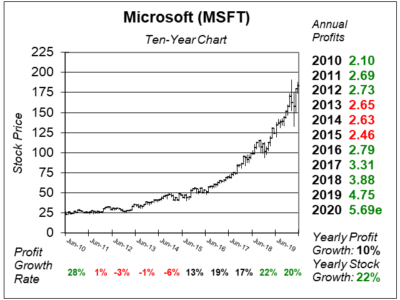

During the 1990s, MSFT would have big bursts of profit growth when a new version of Windows was released, then profit growth would simmer down in the years to follow. Today, the company has more consistent streams of revenue as a lot of its products are sold on a monthly subscription basis. Microsoft has three main divisions, which are listed below, with each bringing in around 1/3rd of revenue. Here’s the breakdown of last qtr’s sales growth by division:

Microsoft is one of the world’s safest stocks, but it’s certainty not a slow grower. As we saw earlier, the company has been delivering mid-teens sales growth. And with the business being software, there’s not a lot of cost-of-goods-sold, thus profits have the ability to grow faster than sales. Management buys back billions in stock and pays a dividend that’s increased every year since 2006. Microsoft’s Est. LTG of 15% per year is good, and the dividend yield is 1%. But right now I consider this company — and perhaps the stock — to be a 25% grower. MSFT is a top holding in the Growth Portfolio, Aggressive Growth Portfolio and Conservative Growth Portfolio. This is a perfect business environment for the company to thrive in. |

One Year Chart |

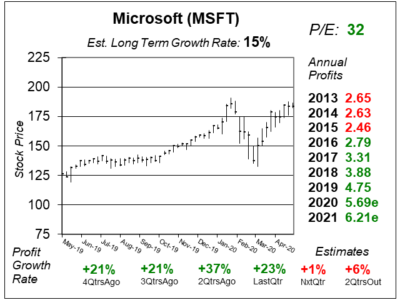

Nice profit growth the last four qtrs. Estimates look poor, but I imagine the company will beat these estimates as business is strong. Nice profit growth the last four qtrs. Estimates look poor, but I imagine the company will beat these estimates as business is strong.

The Est. LTG of 15% is the same as last qtr. Right now this company is growing +20%. The 32 P/E is fine considering the recent profit growth rate. |

Earnings Table |

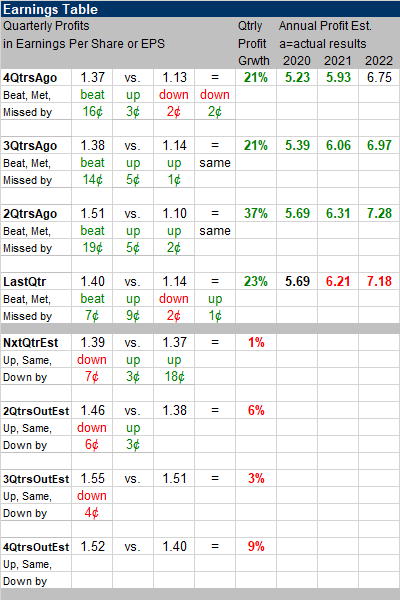

Last qtr MSFT delivered 23% profit growth and beat estimates of 17%. Revenue increased 15%. Last qtr MSFT delivered 23% profit growth and beat estimates of 17%. Revenue increased 15%.

Annual Profit Estimates are similar to last qtr’s. Hmmm. I would have imagined estimates would be higher. Qtrly Estimates are just stupid! Why did estimates decline when the company booked two years worth of business in two months? I think MSFT will continue to deliver ~25% profit growth the next 4 qtrs. |

Fair Value |

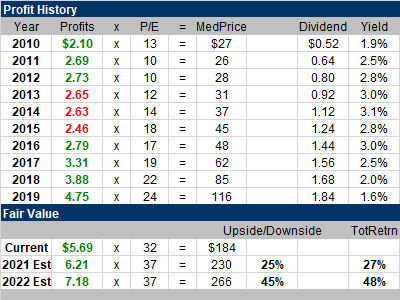

What’s so ridiculous about analysts decreasing profit estimates is 2021’s profit est. is probably reflective of what MSFT will possibly make. That number just went from $6.31 to $6.21. It should have jumped to around $6.50. What’s so ridiculous about analysts decreasing profit estimates is 2021’s profit est. is probably reflective of what MSFT will possibly make. That number just went from $6.31 to $6.21. It should have jumped to around $6.50.

My Fair Value P/E is going up from 35 to 37 to compensate for the lower estimates. Microsoft has its Fiscal Year end of June 30th, so this qtr I’m looking ahead to next year’s profit number (2021) when calculating my Fair Value. Thus, I think the $230 price is achievable within the next year, and $266 is for the year-after. This stock is around its highs right now, but it still has room to run higher. |

Bottom Line |

Microsoft (MSFT) has reinvented itself into dynamic software firm. Microsoft 365, Windows 10, LinkedIn, Xbox, Azure and Dynamics give the company an unmatched array that is the best in the business world. Teams is becoming more popular as it allows employees to work-from-home on an interface that combines chat, video calls, and file sharing. And a new Xbox is on the horizon that should boost the More Personal Computing division (which only had 3% sales growth last qtr). Microsoft (MSFT) has reinvented itself into dynamic software firm. Microsoft 365, Windows 10, LinkedIn, Xbox, Azure and Dynamics give the company an unmatched array that is the best in the business world. Teams is becoming more popular as it allows employees to work-from-home on an interface that combines chat, video calls, and file sharing. And a new Xbox is on the horizon that should boost the More Personal Computing division (which only had 3% sales growth last qtr).

This company is clicking on all cylinders. And with these low qtrly estimates on the horizon, it should be easy for MSFT to beat the street in the coming qtrs. And my bullishness on the stock is good news for the NASDAQ and the stock market overall. MSFT pushed up from 4th to 1st in the Conservative Stock Portfolio Power Rankings. It’s a safe stock that’s growing like a growth stock. The stock continues to rank 5th in the Growth Portfolio and Aggressive Growth Portfolio Power Rankings. |

Power Rankings |

Growth Stock Portfolio

5 of 45Aggressive Growth Portfolio 5 of 22Conservative Stock Portfolio 1 of 31 |