Stock (Symbol) |

MasterCard (MA) |

Stock Price |

$103 |

Sector |

| Financial |

Data is as of |

| January 2, 2017 |

Expected to Report |

| Jan 31 |

Company Description |

MA is a technology company in the global payments industry. MA connects consumers, financial institutions, merchants, Governments and businesses around the world, enabling them to use electronic forms of payment instead of cash and checks. MA brands include MasterCard, Maestro and Cirrus. It provides offerings, such as loyalty and reward programs, information services and consulting. The Company focuses on segments, including Government programs, such as Social Security payments, unemployment benefits; commercial programs, such as payroll, health savings accounts, employee benefits and others, and consumer reloadable programs for individuals without formal banking relationships and non-traditional users of electronic payments. MA provides a variety of products and solutions that support payment products that customers can offer to their cardholders. Source: Thomson Financial MA is a technology company in the global payments industry. MA connects consumers, financial institutions, merchants, Governments and businesses around the world, enabling them to use electronic forms of payment instead of cash and checks. MA brands include MasterCard, Maestro and Cirrus. It provides offerings, such as loyalty and reward programs, information services and consulting. The Company focuses on segments, including Government programs, such as Social Security payments, unemployment benefits; commercial programs, such as payroll, health savings accounts, employee benefits and others, and consumer reloadable programs for individuals without formal banking relationships and non-traditional users of electronic payments. MA provides a variety of products and solutions that support payment products that customers can offer to their cardholders. Source: Thomson Financial |

Sharek’s Take |

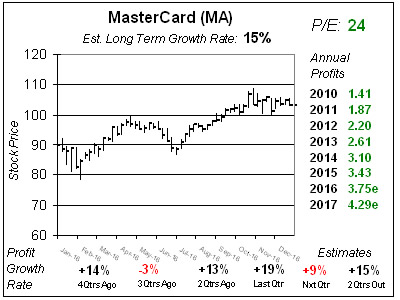

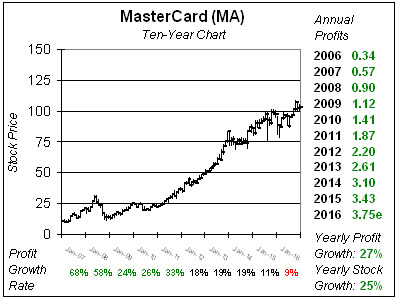

MasterCard (MA) is on a roll as it has beaten the street and had annual profit estimates climb the past three qtrs. During the last three qtrs 2016 profit estimates have climbed from $3.54 to $3.63 and now $3.75. 2017’s estimate has risen from $4.14 to $4.20 and $4.29. These little differences make a big difference over the course of the year, and these bump-ups also signal a healthy business. The company has been experiencing double-digit volume and transaction growth for a while now, but foreign exchange was reducing profits to the point MA will likely grown profits 10% a year the past two years, way less than the decade average of 27% a year. Also, MA gives up-front incentives to banks to garner new business and this hurts profits in the beginning of the deal while helping profits further out. Now MA isn’t a rapid grower like it was years ago, but the Est. LTG is 15% a year and it would be nice if profit growth got back to that level. Qtrly profit Estimates are are for profit growth of 9%, 15%, 14% and 11% the next 4 qtrs — so if MA continues to beat the street perhaps the company can deliver 15% profit growth in 2017. Management also buys back stock, which could give these numbers a boost.MasterCard is a safe stock that pays a yield of just under 1%. This core stock is beloved by mutual fund managers who like long-term growth with large safe companies. Profits have grown every year since the stock went public. I am adding MA to the Conservative Portfolio today and have it on the radar for the Growth Portfolio if it gets down below $100. MasterCard (MA) is on a roll as it has beaten the street and had annual profit estimates climb the past three qtrs. During the last three qtrs 2016 profit estimates have climbed from $3.54 to $3.63 and now $3.75. 2017’s estimate has risen from $4.14 to $4.20 and $4.29. These little differences make a big difference over the course of the year, and these bump-ups also signal a healthy business. The company has been experiencing double-digit volume and transaction growth for a while now, but foreign exchange was reducing profits to the point MA will likely grown profits 10% a year the past two years, way less than the decade average of 27% a year. Also, MA gives up-front incentives to banks to garner new business and this hurts profits in the beginning of the deal while helping profits further out. Now MA isn’t a rapid grower like it was years ago, but the Est. LTG is 15% a year and it would be nice if profit growth got back to that level. Qtrly profit Estimates are are for profit growth of 9%, 15%, 14% and 11% the next 4 qtrs — so if MA continues to beat the street perhaps the company can deliver 15% profit growth in 2017. Management also buys back stock, which could give these numbers a boost.MasterCard is a safe stock that pays a yield of just under 1%. This core stock is beloved by mutual fund managers who like long-term growth with large safe companies. Profits have grown every year since the stock went public. I am adding MA to the Conservative Portfolio today and have it on the radar for the Growth Portfolio if it gets down below $100. |

One Year Chart |

Last qtr MA posted revenue growth of 14% and profit growth of 19%, which blew away estimates of 7% profit growth. In comments to investors, management said the US is on a steady growth path and many markets across Europe are showing gradual recovery. The UK remains stable. In China exports & imports were down sharply. Brazil seems to be bottoming out, things are getting worse in Venezuela, and in Mexico the economy continues to expand. MA’s P/E was 28 last qtr and this qtr it’s 24. The stock is cheaper now, because I’m calculating the P/E based on 2017 profits instead of 2016’s. Last qtr MA posted revenue growth of 14% and profit growth of 19%, which blew away estimates of 7% profit growth. In comments to investors, management said the US is on a steady growth path and many markets across Europe are showing gradual recovery. The UK remains stable. In China exports & imports were down sharply. Brazil seems to be bottoming out, things are getting worse in Venezuela, and in Mexico the economy continues to expand. MA’s P/E was 28 last qtr and this qtr it’s 24. The stock is cheaper now, because I’m calculating the P/E based on 2017 profits instead of 2016’s. |

Fair Value |

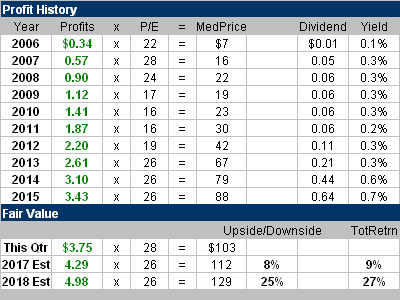

MasterCard has been selling for 26x earnings for a while now. That’s surprising because the profit growth rate slowed from the 20s to the high-teens in 2012 and then to around 10% these past two years. I think investors appreciate the steady growth MA provides. My 2017 Fair Value is $112 and 2018’s is $129. There’s good upside to 2018’s figure. Keep in mind estimates have also been on the rise, thus my Fair Values could increase accordingly. MasterCard has been selling for 26x earnings for a while now. That’s surprising because the profit growth rate slowed from the 20s to the high-teens in 2012 and then to around 10% these past two years. I think investors appreciate the steady growth MA provides. My 2017 Fair Value is $112 and 2018’s is $129. There’s good upside to 2018’s figure. Keep in mind estimates have also been on the rise, thus my Fair Values could increase accordingly. |

Bottom Line |

MasterCard is a solid buy-and-hold stock that provides a good solid base for stock portfolios. MA is a conservative stock that is expected to grow profits at 15% a year, has grown profits each and every year since going public, pays a dividend, and buys back stock. Recently, profits have been hampered by a strong USD and incentives paid our for new business, but the outlook is better for 2017. I will add MA to the Conservative Growth Portfolio where it will rank 16th of 30 stocks in the Power Rankings. MasterCard is a solid buy-and-hold stock that provides a good solid base for stock portfolios. MA is a conservative stock that is expected to grow profits at 15% a year, has grown profits each and every year since going public, pays a dividend, and buys back stock. Recently, profits have been hampered by a strong USD and incentives paid our for new business, but the outlook is better for 2017. I will add MA to the Conservative Growth Portfolio where it will rank 16th of 30 stocks in the Power Rankings. |

Power Rankings |

Growth Stock Portfolio

N/AAggressive Growth Portfolio N/AConservative Growth Portfolio 16 of 30 |