Stock (Symbol) |

Google (GOOGL) |

Stock Price |

$737 |

Sector |

| Technology |

Data is as of |

| October 29, 2015 |

Expected to Report |

| N/A |

Company Description |

Google Inc. (Google) is a global technology company focused on improving the ways people connect with information. The Company generates revenue primarily by delivering online advertising. As of December 31, 2011, the Company’s business was focused on areas, such as search, advertising, operating systems and platforms, and enterprise. Businesses use its AdWords program to promote their products and services with targeted advertising. In addition, the third parties that comprise the Google Network use its AdSense program to deliver relevant advertisements that generate revenue. Source: Thomson Financial Google Inc. (Google) is a global technology company focused on improving the ways people connect with information. The Company generates revenue primarily by delivering online advertising. As of December 31, 2011, the Company’s business was focused on areas, such as search, advertising, operating systems and platforms, and enterprise. Businesses use its AdWords program to promote their products and services with targeted advertising. In addition, the third parties that comprise the Google Network use its AdSense program to deliver relevant advertisements that generate revenue. Source: Thomson Financial |

Sharek’s Take |

Google (GOOGL) is doing things right and the stock’s benefiting. For the second straight qtr expense control helped push the stock higher after the company reported earnings. Profits increased 16% last qtr, on a 13% rise in sales. Earnings grew faster than sales due to just a 9% increase in total costs. As an added bonus the company announced a $5 billion stock buyback plan. I used to have a negative stance on management years ago, and now that’s reversed course. I think the company is doing things in the interest of shareholders. But my 2016 Fair Value is $786 and that’s what the stock’s selling for today. GOOGL is a good buy-and-hold investment, but with the stock at its highs one could wait and try to get it on a dip. Note: these charts are as of 10/29. Google (GOOGL) is doing things right and the stock’s benefiting. For the second straight qtr expense control helped push the stock higher after the company reported earnings. Profits increased 16% last qtr, on a 13% rise in sales. Earnings grew faster than sales due to just a 9% increase in total costs. As an added bonus the company announced a $5 billion stock buyback plan. I used to have a negative stance on management years ago, and now that’s reversed course. I think the company is doing things in the interest of shareholders. But my 2016 Fair Value is $786 and that’s what the stock’s selling for today. GOOGL is a good buy-and-hold investment, but with the stock at its highs one could wait and try to get it on a dip. Note: these charts are as of 10/29. |

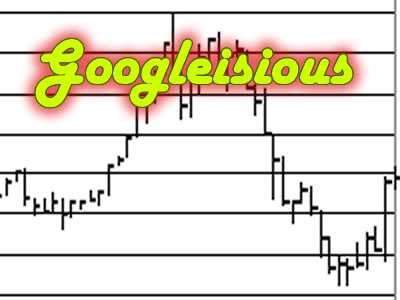

One Year Chart |

GOOGL’s posted two break outs now in two qtrs. Outstanding. But notice profit growth is in the high-teens, which is good but not great. The company has beaten analyst estimates by a little the last two qtrs, and the annual estimates are ticking higher. My Fair Value is 23x earnings and that’s what GOOGL’s selling for now. GOOGL’s posted two break outs now in two qtrs. Outstanding. But notice profit growth is in the high-teens, which is good but not great. The company has beaten analyst estimates by a little the last two qtrs, and the annual estimates are ticking higher. My Fair Value is 23x earnings and that’s what GOOGL’s selling for now. |

Fair Value |

Maybe this stock will now garner a higher valuation from institutional investors now that it’s doing things right. Today I overheard a $1000 target price put out by someone. If the company makes around $35 next year that would be 29x earnings. Hmmm. I think that’s too much to ask. Unless profit growth picks up to +20% which when you look at Estimates in the one-year chart (above) seems possible. Maybe this stock will now garner a higher valuation from institutional investors now that it’s doing things right. Today I overheard a $1000 target price put out by someone. If the company makes around $35 next year that would be 29x earnings. Hmmm. I think that’s too much to ask. Unless profit growth picks up to +20% which when you look at Estimates in the one-year chart (above) seems possible. |

Bottom Line |

Google has been a tough stock to handle the past few years. What has happened a few times is the stock’s gapped up after earnings, surprising us. Google has been a tough stock to handle the past few years. What has happened a few times is the stock’s gapped up after earnings, surprising us.

Google is not doing things right and the stock is trending higher. But with profits expected to grow 18% on average the next four qtrs the stock seems fairly valued here at 23x earnings. GOOGL is ranked 3rd in the Conservative Growth Portfolio Power Rankings. I will look to buy it back in the Growth Portfolio if it dips. |

Power Rankings |

Growth Stock Portfolio

N/AAggressive Growth Portfolio N/AConservative Stock Portfolio 3 of 30 |