Stock (Symbol) |

Becton, Dickinson (BDX) |

Stock Price |

$168 |

Sector |

| Healthcare |

Data is as of |

| January 6, 2017 |

Expected to Report |

| Feb 1 – 6 |

Company Description |

BDX is a global medical technology company engaged in the development, manufacture and sale of a range of medical supplies, devices, laboratory equipment and diagnostic products used by healthcare institutions, life science researchers, clinical laboratories. The Company operates through two segments: BD Medical and BD Life Sciences. The Company’s Life Sciences segment consists of the BD Diagnostics and BD Biosciences segments. The Company’s BD Medical segment focuses on providing solutions to reduce the spread of infection, enhance diabetes treatment and advance drug delivery. The Company’s BD Diagnostics provides products for the safe collection and transport of diagnostics specimens, as well as instruments and reagent systems. Its BD Biosciences provide diagnostic and research tools to life science researchers, clinical researchers, laboratory professionals and clinicians. Source: Thomson Financial BDX is a global medical technology company engaged in the development, manufacture and sale of a range of medical supplies, devices, laboratory equipment and diagnostic products used by healthcare institutions, life science researchers, clinical laboratories. The Company operates through two segments: BD Medical and BD Life Sciences. The Company’s Life Sciences segment consists of the BD Diagnostics and BD Biosciences segments. The Company’s BD Medical segment focuses on providing solutions to reduce the spread of infection, enhance diabetes treatment and advance drug delivery. The Company’s BD Diagnostics provides products for the safe collection and transport of diagnostics specimens, as well as instruments and reagent systems. Its BD Biosciences provide diagnostic and research tools to life science researchers, clinical researchers, laboratory professionals and clinicians. Source: Thomson Financial |

Sharek’s Take |

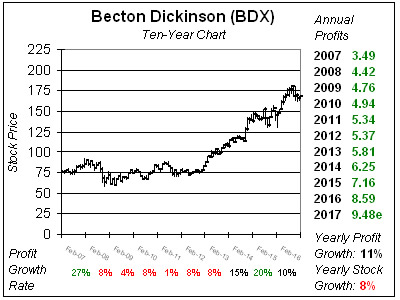

Becton, Dickinson (BDX) has manufactured syringes, catheters, lab equipment, diagnostic tests, and other disposable items for hospitals since 1897. What had been seen as a 8% to 10% grower, BDX kicked profit growth up a notch in 2015 when it acquired CareFusion, a maker of precision drug dispensing equipment. This merger boosted profit growth from around 10% to 20% in fiscal 2016 (year ending Sept 30th) as CareFusion gives Becton, Dickinson a more complete menu of medical products to hospitals. Additionally, Becton can also use its deep International network to sell CareFusion products, which in the past had just a limited presence abroad. But now that the merger is more than a year old, profit growth has returned to more normalized levels. Also, the company had been whipping earnings estimates, but only beat by a little last qtr. The slowdown in growth has taken the momentum out of this stock. BDX had a nice run from $150 to $180 during 2016, and has since has settled down to the $170 area. Still, Becton, Dickinson has grown profits every year going back to at least the year 2000, has an Estimated Long Term Growth Rate of 10% a year and a 2% yield. The dividend has increased every year since 1972. This is a nice safe stock for conservative investors. Becton, Dickinson (BDX) has manufactured syringes, catheters, lab equipment, diagnostic tests, and other disposable items for hospitals since 1897. What had been seen as a 8% to 10% grower, BDX kicked profit growth up a notch in 2015 when it acquired CareFusion, a maker of precision drug dispensing equipment. This merger boosted profit growth from around 10% to 20% in fiscal 2016 (year ending Sept 30th) as CareFusion gives Becton, Dickinson a more complete menu of medical products to hospitals. Additionally, Becton can also use its deep International network to sell CareFusion products, which in the past had just a limited presence abroad. But now that the merger is more than a year old, profit growth has returned to more normalized levels. Also, the company had been whipping earnings estimates, but only beat by a little last qtr. The slowdown in growth has taken the momentum out of this stock. BDX had a nice run from $150 to $180 during 2016, and has since has settled down to the $170 area. Still, Becton, Dickinson has grown profits every year going back to at least the year 2000, has an Estimated Long Term Growth Rate of 10% a year and a 2% yield. The dividend has increased every year since 1972. This is a nice safe stock for conservative investors. |

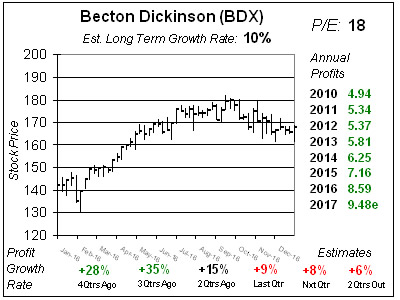

One Year Chart |

You can see the momentum leaving these shares in the one-year chart as Becton, Dickinson returns to more normalized growth. Last qtr BDX’s had 5% sales growth and turned that into 9% profit growth, which beat the 8% estimate. Afterwards, analysts kept profit estimates rather steady. Qtrly profit Estimates now stand at 8%, 6%, 9% and 18%. The Est. LTG is down from 13% to 10% since last qtr. The P/E of 18 is reasonable. You can see the momentum leaving these shares in the one-year chart as Becton, Dickinson returns to more normalized growth. Last qtr BDX’s had 5% sales growth and turned that into 9% profit growth, which beat the 8% estimate. Afterwards, analysts kept profit estimates rather steady. Qtrly profit Estimates now stand at 8%, 6%, 9% and 18%. The Est. LTG is down from 13% to 10% since last qtr. The P/E of 18 is reasonable. |

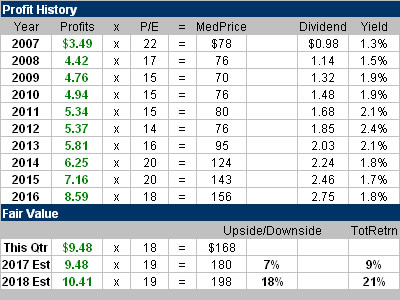

Fair Value |

My Fair Value is 19x earnings, down from 20x last qtr. I feel I might make it 18x next qtr now that profit growth has slowed. Notice this stock had a P/E of around 15 from 2009-2013, but value stocks like BDX had lower valuations during that time. BDX has decent upside for 2017, when you include the dividend and factor the safety rating in. My Fair Value is 19x earnings, down from 20x last qtr. I feel I might make it 18x next qtr now that profit growth has slowed. Notice this stock had a P/E of around 15 from 2009-2013, but value stocks like BDX had lower valuations during that time. BDX has decent upside for 2017, when you include the dividend and factor the safety rating in. |

Bottom Line |

Becton, Dickinson got jolt of energy with CareFusion But now the company is experiencing more normalized growth, which means a lower valuation (P/E). Now this stock is more of a buy-and-hold investment for conservative investors and trust accounts. I love the fact profits have grown every year since 2000, but you have to be comfortable with 8% as profit growth has been 8% in 4 of the last 8 years and the stock has compounded at 8% a year the last decade. But when you tack on a 2% yield, 8% would be a welcome return for investors in need of growth & safety. BDX ranks 22nd of 30 stocks in the Conservative Portfolio Power Rankings. Becton, Dickinson got jolt of energy with CareFusion But now the company is experiencing more normalized growth, which means a lower valuation (P/E). Now this stock is more of a buy-and-hold investment for conservative investors and trust accounts. I love the fact profits have grown every year since 2000, but you have to be comfortable with 8% as profit growth has been 8% in 4 of the last 8 years and the stock has compounded at 8% a year the last decade. But when you tack on a 2% yield, 8% would be a welcome return for investors in need of growth & safety. BDX ranks 22nd of 30 stocks in the Conservative Portfolio Power Rankings. |

Power Rankings |

Growth Stock Portfolio

N/AAggressive Growth Portfolio N/AConservative Stock Portfolio 22 of 30 |