Stock (Symbol) |

Align Technology (ALGN) |

Stock Price |

$179 |

Sector |

| Healthcare |

Data is as of |

| September 5, 2017 |

Expected to Report |

| Oct 26 |

Company Description |

Align Technology, Inc. designs, manufactures and markets a system of clear aligner therapy, intra-oral scanners and computer-aided design/computer-aided manufacturing (CAD/CAM) digital services used in dentistry, orthodontics and dental records storage. Source: Thomson Financial Align Technology, Inc. designs, manufactures and markets a system of clear aligner therapy, intra-oral scanners and computer-aided design/computer-aided manufacturing (CAD/CAM) digital services used in dentistry, orthodontics and dental records storage. Source: Thomson Financial |

Sharek’s Take |

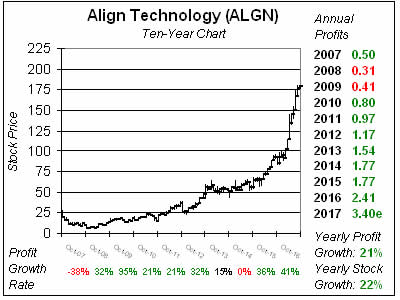

Align Technology is having a fabulous year. Align is the company that designs and manufactures Invisalign clear braces and iTero scanners, which dentists use to scan teeth for a fitting. This stock has doubled in the last year and is one of the hottest in the market. But is it too late to buy? I think so. Still, the numbers here are rock solid, so I also expect the shares to continue higher. Here’s some highlights from last qtr: Align Technology is having a fabulous year. Align is the company that designs and manufactures Invisalign clear braces and iTero scanners, which dentists use to scan teeth for a fitting. This stock has doubled in the last year and is one of the hottest in the market. But is it too late to buy? I think so. Still, the numbers here are rock solid, so I also expect the shares to continue higher. Here’s some highlights from last qtr:

Align also supplies clear aligners to SmileDirectClub, and has a 19% stake in the company. SmileDirectClub is an at-home doctor-directed program which is less expensive than the regular routine. And two qtrs ago ALGN launched a lighter version of its braces, called Invisalign Light, which includes up to 14 stage aligners vs 40 or more sets in Invisalign when teeth are more crooked. This could prove to be a future catalyst for a company that doesn’t seem to need it. ALGN is one of the top stocks on the market, but sells for a rich 53 times earnings. And to be frank, this stock is always expensive. I let the stock take off without me when it was in the $90s earlier in the year, and have obviously regretted it. But now the stock is parabolic on the ten year chart and I feel it’s more prudent to wait for a correction to buy in. |

One Year Chart |

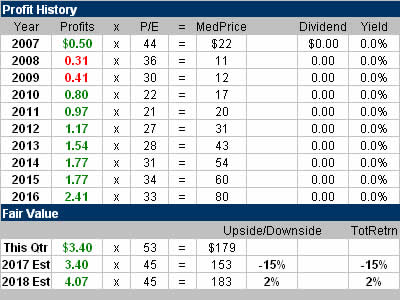

Sales growth of 32% and profit growth of 37% last qtr. Profit estimates were just 18% and the company whipped that figure. Also, profit estimates climbed across the board this qtr, with 2017’s est rising from $3.19 to $3.40. Qtrly profit Estimates are 27%, 33%, 44% and 20%. ALGN could grow profits 50% or more the next few qtrs. But that news is priced in as the P/E is 53. Nice Est. LTG of 26% a year. Sales growth of 32% and profit growth of 37% last qtr. Profit estimates were just 18% and the company whipped that figure. Also, profit estimates climbed across the board this qtr, with 2017’s est rising from $3.19 to $3.40. Qtrly profit Estimates are 27%, 33%, 44% and 20%. ALGN could grow profits 50% or more the next few qtrs. But that news is priced in as the P/E is 53. Nice Est. LTG of 26% a year. |

Fair Value |

My Fair Value is a P/E of 45. That gives me a Fair Value of $153 and honestly I’d love to buy in at that price. 2018’s FV is $183 but since annual estimates just jumped I think it’s possible this company could make $5 next year, and a P/E of 45 on that figure would be a $210 stock. Hypothetically of course. My Fair Value is a P/E of 45. That gives me a Fair Value of $153 and honestly I’d love to buy in at that price. 2018’s FV is $183 but since annual estimates just jumped I think it’s possible this company could make $5 next year, and a P/E of 45 on that figure would be a $210 stock. Hypothetically of course. |

Bottom Line |

Align Technologies is one of the best stocks in the market, but after a tremendous run the stock has gone parabolic and is dangerous to buy here. The problem is now I have to wait for a pullback to get in, and that seems unlikely with the solid sales numbers that are coming in. ALGN is on the top of my radar, but I feel we need a stock market correction for this stock to fall to a buyable level. If it were too I would likely add it to the Growth Portfolio and Aggressive Growth Portfolio around $155. Align Technologies is one of the best stocks in the market, but after a tremendous run the stock has gone parabolic and is dangerous to buy here. The problem is now I have to wait for a pullback to get in, and that seems unlikely with the solid sales numbers that are coming in. ALGN is on the top of my radar, but I feel we need a stock market correction for this stock to fall to a buyable level. If it were too I would likely add it to the Growth Portfolio and Aggressive Growth Portfolio around $155. |

Power Rankings |

Growth Stock Portfolio

N/AAggressive Growth Portfolio N/AConservative Stock Portfolio N/A |