Stock (Symbol) |

Stryker (SYK) |

Stock Price |

$120 |

Sector |

| Healthcare |

Data is as of |

| January 2, 2017 |

Expected to Report |

| Jan 24 – 30 |

Company Description |

Stryker Corporation (Stryker) is a medical technology company. The Company operates through three segments: Orthopaedics, MedSurg, and Neurotechnology and Spine. The Company’s Orthopaedics segment products consist of implants used in hip and knee joint replacements and trauma and surgeries. The Company’s MedSurg segment products consist of surgical equipment and surgical navigation systems (Instruments); endoscopic and communications systems (Endoscopy); patient handling and emergency medical equipment (Medical), and reprocessed and remanufactured medical devices (Sustainability), as well as other medical device products used in a range of medical specialties. The Company’s Neurotechnology and Spine segment products consist of both neurosurgical and neurovascular devices. The Company’s products are sold in approximately 100 countries through the Company-owned sales subsidiaries and branches, as well as third-party dealers and distributors. Source: Thomson Financial Stryker Corporation (Stryker) is a medical technology company. The Company operates through three segments: Orthopaedics, MedSurg, and Neurotechnology and Spine. The Company’s Orthopaedics segment products consist of implants used in hip and knee joint replacements and trauma and surgeries. The Company’s MedSurg segment products consist of surgical equipment and surgical navigation systems (Instruments); endoscopic and communications systems (Endoscopy); patient handling and emergency medical equipment (Medical), and reprocessed and remanufactured medical devices (Sustainability), as well as other medical device products used in a range of medical specialties. The Company’s Neurotechnology and Spine segment products consist of both neurosurgical and neurovascular devices. The Company’s products are sold in approximately 100 countries through the Company-owned sales subsidiaries and branches, as well as third-party dealers and distributors. Source: Thomson Financial |

Sharek’s Take |

Stryker develops orthopedic implants, surgical equipment, neurotechnology and spine products. Stryker has compiled 37 straight years of record sales growth and is cash rich. The company uses its money wisely. It buys back stock, pay a dividend, and make acquisitions — I love three-pronged attacks like this. It’s had dividend growth of 15% per year since 2012. Stryker develops orthopedic implants, surgical equipment, neurotechnology and spine products. Stryker has compiled 37 straight years of record sales growth and is cash rich. The company uses its money wisely. It buys back stock, pay a dividend, and make acquisitions — I love three-pronged attacks like this. It’s had dividend growth of 15% per year since 2012.

Stryker has three main divisions:

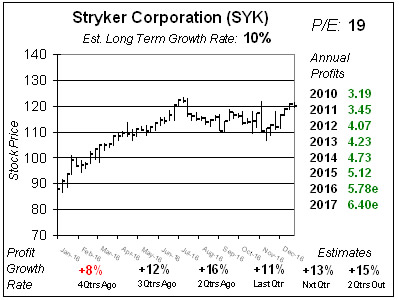

Of the 17% sales growth SYK delivered last qtr, 11% was from acquisitions with 6% organic growth. Management targets profit growth of at least 9% annually, and analysts peg the Est. LTG at 10% a year. Tack on a 1.4% dividend and this safe stock has the ability to provide double-digit returns. Although SYK is up from around $90 to $120 in the past year, I think the momentum will continue as profits are expected to climb an average of 13% a qtr the next 4 qtrs. At 19x earnings, Stryker is reasonably priced. My 2017 Fair Value is currently $128. 2018’s is $140. |

One Year Chart |

Stryker produced 17% profit growth last qtr, with 11% profit growth, which beat the 10% estimate. Future estimates didn’t adjust much. The company now has a nice streak of three straight qtrs of double-digit profit growth, and Estimates call for that to continue the next 4 qtrs. Overall, profit Estimates for the next 4 qtrs are 13%, 15%, 11% and 11%. The P/E of 19 is reasonable. Stryker produced 17% profit growth last qtr, with 11% profit growth, which beat the 10% estimate. Future estimates didn’t adjust much. The company now has a nice streak of three straight qtrs of double-digit profit growth, and Estimates call for that to continue the next 4 qtrs. Overall, profit Estimates for the next 4 qtrs are 13%, 15%, 11% and 11%. The P/E of 19 is reasonable. |

Fair Value |

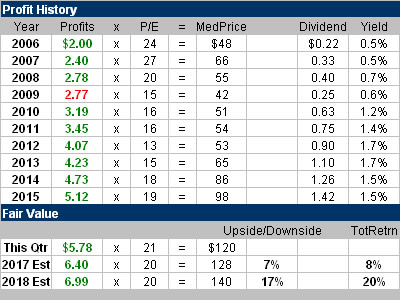

My Fair Value is 20x earnings, which gives the stock modest upside for 2017. Would be nice if the stock could get to $140 by the end of next year, which with dividends would mean a total return of around 20%. My Fair Value is 20x earnings, which gives the stock modest upside for 2017. Would be nice if the stock could get to $140 by the end of next year, which with dividends would mean a total return of around 20%. |

Bottom Line |

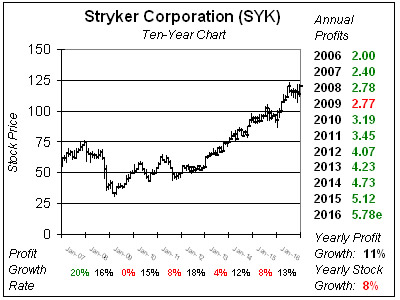

Stryker is a solid stock for conservative investors who yearn for growth with safety. Management does a great job acquiring other companies and bringing those products into Stryker’s lineup. And when there’s no good acquisitions to make, management buys back stock instead. If projections hold true, 2017 would be the first time SYK has grown profits in the double-digits two years straight since 2007-2008. Overall, Stryker is a good investment, but getting it on a dip would be even better as the stock is just 7% away from its 2017 Fair Value. SYK ranks 19th of 30 stocks in the Conservative Portfolio Power Rankings. Stryker is a solid stock for conservative investors who yearn for growth with safety. Management does a great job acquiring other companies and bringing those products into Stryker’s lineup. And when there’s no good acquisitions to make, management buys back stock instead. If projections hold true, 2017 would be the first time SYK has grown profits in the double-digits two years straight since 2007-2008. Overall, Stryker is a good investment, but getting it on a dip would be even better as the stock is just 7% away from its 2017 Fair Value. SYK ranks 19th of 30 stocks in the Conservative Portfolio Power Rankings. |

Power Rankings |

Growth Stock Portfolio

N/AAggressive Growth Portfolio N/AConservative Stock Portfolio 19 of 30 |